The market’s fixation with drug manufacturers involved in treating or preventing the novel coronavirus is creating opportunities for value investors. Pfizer (NYSE:PFE), through its partnership with BioNTech SE (NASDAQ:BNTX), drew in investor interest. Between November and December, PFE stock traded no lower than $34 and topped around $43.

Pfizer separated its off-patent branded drugs business and combined it with Mylan in November. Viatris (NYSE:VTRS) started trading on the New York Stock Exchange on Nov. 13.

So, what is the gameplay with investing in PFE stock?

PFE Stock Has Deep Value

Trading at a forward price-to-earnings of around 12.5 times, Pfizer trades in deep value territory. The stock spent much of the last half-decade (since 2016) in the $30 to $35 range. Every time the stock rallied above $40, the market would find a reason to sell.

The Viatris spinoff is a positive development. The unit will cut up to 15 manufacturing sites globally and reduce its workforce by up to 20%. By simplifying its business structure, Pfizer has one less worry. Shareholders get 57% of the outstanding shares of Viatris. The unit’s value is independent of Pfizer’s prospects.

Pfizer may focus on its partnership with BioNTech in the near term. It paid BNTX an upfront payment of $185 million, which includes a $113 million equity investment. And since BNTX stock performed so well in the year, Pfizer at least has paper gains on its balance sheet. After BNTX received approval from regulatory authorities for its novel coronavirus vaccine, it is on the path of getting milestone payments worth $748 million.

The companies stand to bring in around $13 billion in global sales in the next year. This assumes a price of $39 per two-shot course or $19.50 per dose.

Competition for Vaccine

Pfizer and BioNTech face competition from Johnson & Johnson (NYSE:JNJ) and AstraZeneca (NYSE:AZN). J&J cut the size of its study because of the pervasiveness across the U.S. Investors may interpret the change as benefiting Pfizer-BioNTech. The more subjects a study has, the more durable the results. Still, if J&J’s 38,000 subject count delivers statistically significant results, governments may approve its vaccine, too.

For AstraZeneca, initial confusion over the efficacy of its vaccine may hurt sales. This would benefit Pfizer and BNTX.

Mixed Pfizer’s Third-Quarter Results

Besides its endeavors in the vaccine, Pfizer’s third-quarter results do not inspire investors to accumulate shares. Revenue fell by 4% to $12.131 billion. Net income fell 71% to $2.19 billion, or 39 cents a share. On the conference call, Pfizer’s Chief Financial Officer Frank D’Amelio said he company will use the $12 billion it gets from forming Viatris to pay down debt.

Returning capital to shareholders is a positive development. It will do so without cutting back on its mergers and acquisitions investment. Investors may assume that Pfizer will not cut its research and development activities, either. These activities will nurture its pipeline of potential new drugs ahead. Its mRNA vaccine candidate (with BioNTech) is the most obvious example.

Its Duchenne muscular dystrophin gene therapy product is in Phase 1b. It has an investigational gene therapy for hemophilia A patients. This is a project in partnership with Sangamo. Pfizer announced the first dosage in the Phase 3 AFFINE study on Oct. 7.

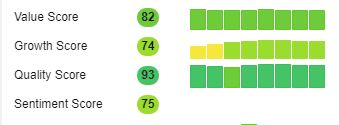

Fair Value

Pfizer scores well on all three key metrics:

Pfizer’s stock score is green on all metrics.

Based on those results, the fair value for Pfizer stock is nearly $48. This is above the average price of $41.54 target (as compiled by Tipranks). In a 5Y DCF EBITDA Exit model, readers may assume a terminal EBITDA multiple of below 12 times. With that metric, the stock has a fair value of at least $42.

| (USD in millions) | Input Projections | |||||

| Fiscal Years Ending | 19-Dec | 20-Dec | 21-Dec | 22-Dec | 23-Dec | 24-Dec |

| Revenue | 51,750 | 48,402 | 49,471 | 48,100 | 49,062 | 50,043 |

| % Growth | -3.50% | -6.50% | 2.20% | -2.80% | 2.00% | 2.00% |

| EBITDA | 21,014 | 20,913 | 23,060 | 21,601 | 22,033 | 22,474 |

| % of Revenue | 40.60% | 43.20% | 46.60% | 44.90% | 44.90% | 44.90% |

Above are the revenue growth assumptions I inputted. Readers may click on this model to change the discount rate and annual revenue changes to re-calculate the fair value. All of the fair value targets listed suggest that PFE stock is an inexpensive value play.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Chris Lau is a contributing author for InvestorPlace.com and numerous other financial sites. Chris has over 20 years of investing experience in the stock market and runs the Do-It-Yourself Value Investing Marketplace on Seeking Alpha. He shares his stock picks so readers get original insight that helps improve investment returns.