General Electric (NYSE:GE) suffered one of the worst performances last week. GE stock enjoyed an uninterrupted uptrend that began in August 2019 and rallied through February 2020. But that ended when a sharp market selloff began.

Worsening market conditions, primarily in the aerospace industry, suggest that General Electric will underperform in the near term. But for buy-and-hold investors, the weakness in GE’s business is only a blip.

Expect the business — and GE stock — to recover over the long haul.

Weakness at GE Aviation

Once a source of General Electric’s growth, GE Aviation will underperform as demand for jet engines drops. The coronavirus from China will freeze airplane production as airline traffic stalls.

What does this mean for GE? The global airline industry will need to cut back capacity and pause flight traffic for a few weeks, at the very least. The world has no idea how long the hardest-hit countries will need to ban flights. Until infection rates fall sharply, GE Aviation will need to draw down its credit line to stay afloat.

Eventually, sales of airplane engines will resume. But the short-term uncertainties will hurt GE stock.

Long-term investors may accumulate shares as the stock falls to discount the risks ahead. And since normalcy will return in the airline industry, the segment is bound to recover.

Growth in GE Health

Due to a shortage of ventilators, GE is ramping up production. It is hiring manufacturing staff and re-allocating staff support to increase ventilator output. Components shortages may limit GE’s output, but if it secures more ceramic capacitors, the company’s health division may increase sales.

The U.S. Federal Trade Commission’s clearance of the biopharma business sale is a positive development. General Electric will receive $21.4 billion, which the company needs to lower its leverage and to improve its balance sheet. GE will lose the $3 billion in revenue the unit produced. But the long-term debt exposed investors to too much risk. Even though the Federal Reserve cut interest rates to zero, GE still needed to de-risk.

CEO Lawrence Culp said that “the value from this transaction will fortify our considerable sources to de-risk our balance sheet and continue to solidify our financial position.”

Given the increasing uncertainties ahead in the global economy, GE shareholders will benefit from a simplified business structure and less debt on the company’s balance sheet.

Further, the CEO said that the company is “focused on protecting the safety of our people, serving our customers in this critical time of need, and continuing to strengthen our businesses.”

So, pivoting toward the production of live-saving healthcare machines will earn the company goodwill. It also adds much-needed revenue to its quarterly performance. The company may pay down its debt with the cash flow while offsetting its aerospace underperformance.

My Valuation on GE Stock

Fifteen analysts have an average price target of $12.42. Long-time bear Stephen Tusa, an analyst at JPMorgan, upgraded the stock to a “hold” rating and has an $8 price target.

And SimplyWall.St number-crunched a $20.75 fair value on GE stock, based on its future cash flow. Yet the site also flagged that interest payments are not covered well by the company’s earnings. Stock Rover also noted the underperformance of GE stock through much of the year.

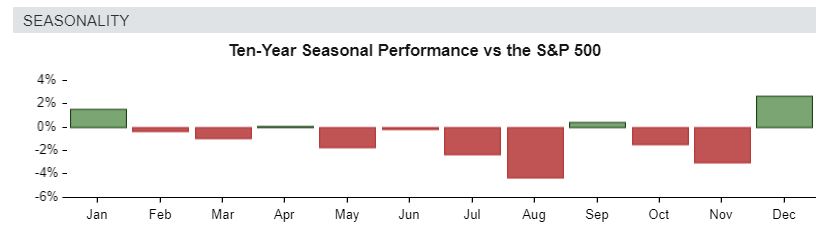

Shares tend to outperform the S&P 500 only in January, September and December.

Still, investors may come up with a price target in the double-digit range on finbox.io. This is based on a bullish earnings before interest, taxes, depreciation and amortization (EBITDA) multiple.

In light of the wide price target ranges on GE stock, expect plenty of volatility ahead. Until uncertainties dissipate, the stock’s trading range will vary. Use the downtrend to accumulate a starting position.

Chris Lau is a contributing author for InvestorPlace.com and numerous other financial sites. Chris has over 20 years of investing experience in the stock market and runs the Do-It-Yourself Value Investing Marketplace on Seeking Alpha. He shares his stock picks so readers get original insight that helps improve investment returns. As of this writing, Chris did not hold a position in any of the aforementioned securities.