Many will argue there’s a very large disconnect between the stock market and the economy. And in a very different way that’s certainly true with Energy Transfer LP (NYSE:ET). But rather than using the opportunity to take profits, is now the time to bet on a return to normalcy for ET stock? Let’s look at what’s happening off and on the price chart to reach a more informed, risk-adjusted conclusion.

It has been a terrific couple of months for risk assets and long equities. The broad-based, large-cap S&P 500 is up nearly 40% since its historic bear market bottom on March 23, 2020. The index is now only a handful of percentage points of wiping its hands clean of the novel coronavirus selloff that began at the tail end of February. And of course, there’s Home Depot (NYSE:HD) or Facebook (NASDAQ:FB), which have delighted bulls even more.

The rally has been even more dazzling for many as today’s forward and very optimistic-looking market has seemingly ignored the Covid-19 crisis, which is still far from over. And more recently, it has turned a blind eye from the polarizing and sometimes violent protesting in the wake of the senseless death of George Floyd.

Blame or applaud the Federal Reserve, but in a market made up of stocks, it would be a mistake to see that same disconnect in shares of Energy Transfer.

In a very different way, oil and gas midstream outfit Energy Transfer decoupled itself from the broader market well before the coronavirus ever became front page news and began impacting our global socioeconomic fabric. ET stock is down 63% since reaching an all-time-high five years ago. Shares were also already down nearly 50% leading into 2020. The lengthy weakness in the stock is hardly surprising either.

Along with steadily declining oil and natural gas prices over the last few years and way too many supply and demand issues to bother counting, the coronavirus was only the final straw to push those commodities over the edge and enable multi-decade, record lows. Given the circumstances, some might question if this is the end of the road. And it might be, but in a very good way, at last for ET stock.

As InvestorPlace’s Mark Hake recently noted after crunching the numbers, Energy Transfer has what it takes to move higher. Moreover, the case is made to purchase shares as its historically large distribution not only pays investors for their commitment, but also supports a rising share price.

Currently, Energy Transfer pays shareholders about 15% compared to a historical average of 10.5%. A return towards more normalized distribution levels would mean the stock is currently undervalued by roughly 42%.

Should investors be worried Energy Transfer’s hefty distribution stream is poorly funded and a trap in-the-making? It would be ignorant not to worry. But, again, the company’s financial position and pledged actions to reduce its capex costs strongly suggest otherwise.

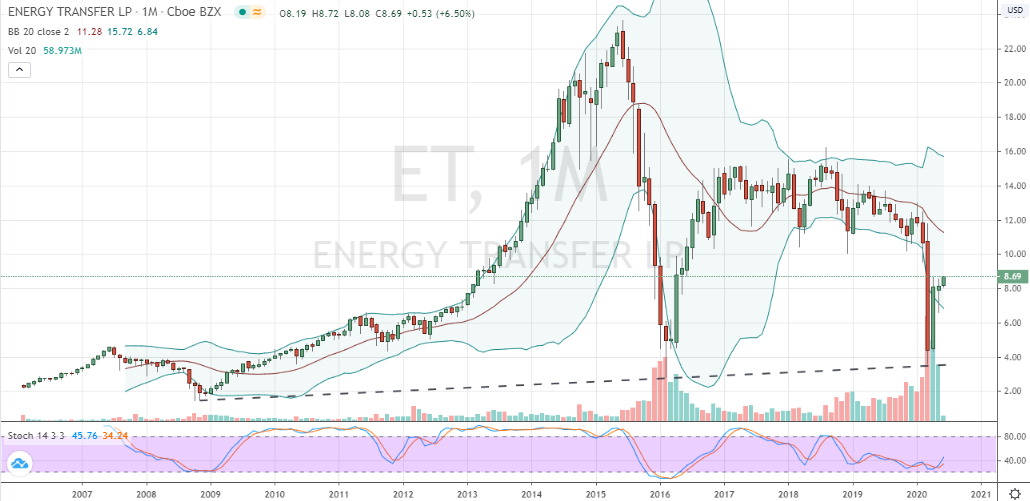

ET Stock Price Monthly Chart

Source: Charts by TradingView

On the price chart for ET stock, the argument for owning Energy Transfer is also building favorably for investors. Aside from providing portfolio diversification given the stock’s overall low correlation the past few years, today’s market offers investors a timely entry as well.

This view differs from Hake’s proffered approach to buy shares on weakness. The reason being, Energy Transfer has already, and for some time now, been weak. As alluded to before, that’s why today’s near-15% yield exists.

More recently, shares have been just spirited enough technically to form a bullishly diverging double-bottom pattern off the stock’s life-time support line. Not only has the price action proven bullish relative to energy markets, now Energy Transfer is signaling a buy confirmation, as the stock trades through the high of its bottoming candle.

Ultimately, today’s the time to buy ET stock based on the evidence both off and on the price chart. And, respectfully, waiting for a pullback at this juncture is simply a much riskier play.

Disclosure: Investment accounts under Christopher Tyler’s management do not currently own positions in any securities mentioned in this article. The information offered is based upon Christopher Tyler’s observations and strictly intended for educational purposes only; the use of which is the responsibility of the individual. For additional options-based strategies, related musings or to ask a question, you can find and follow Chris on Twitter @Options_CAT and StockTwits.