Chevron (NYSE:CVX) is on the rise, with Chevron stock gaining more than 6% over the last month. That’s excellent news as the American multinational energy corporation battles on several fronts to minimize the damage caused by the novel coronavirus pandemic.

As the world grapples with Covid-19, oil prices have taken a substantial dip in recent months. In addition, geopolitics is also weighing heavily on the sector, as production increases from Saudi Arabia have not helped matters.

The U.S. has urged members of OPEC+ to maintain production cuts to shore up oil prices. OPEC+ and its allies agreed to extend the cuts by another month.

The move makes sense, as global oil demand is down as much as 20% year over year. Countries are trying to contain the virus by keeping billions under lockdown. Even as states ease restrictions, it will take a while before oil demand is back to pre-pandemic levels.

However, these are issues that are out of Chevron’s hands – it can only hope oil prices return start to move northward as we move further along in the year. In the interim, Chevron is maintaining a pristine balance sheet, cutting its capital expenditures, and has a stable dividend policy. It also helps that the company is not highly encumbered, making capital raising easier.

All of these factors make me believe CVX stock will continue to gain as we move further along the path to recovery.

Low Debt-Equity Ratio Gives Chevron Leverage

Balance sheet strength is key for any company wishing to come out of this crisis with a degree of stability. Chevron is doing an excellent job in this regard vis-à-vis its competition.

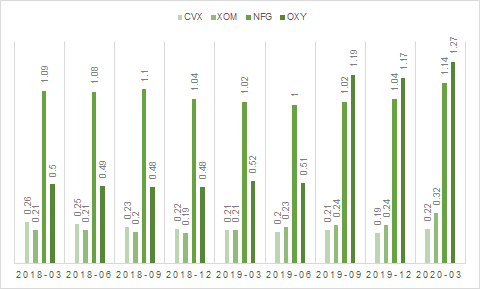

In its recently concluded quarter, the company finished with a debt-equity ratio of 0.22. That’s the lowest when pitted against three competitors that I examined – Exxon Mobil (NYSE:XOM), National Fuel Gas (NYSE:NFG), and Occidental Petroleum (NYSE:OXY).

Since Chevron has the least amount of debt on its balance sheet, it leaves the door open for it to tap debt markets for more dry powder. Recently, S&P Global Ratings changed its outlook on the company from negative to stable. In a note, the credit rating agency said the change in outlook reflects the belief that “the supermajor will maintain modest financial policies that will support sustainably improved financial performance.”

S&P also affirmed the company’s “AA” ratings, underscoring the ease of access Chevron has to low-cost debt.

Dividends Are Strong and Stable

Exxon Mobil and Chevron are the only two oil companies on the list of S&P “dividend aristocrats,” companies that have raised their dividends every year for at least 25 consecutive years. It’s unlikely that the companies will maintain this record in 2020, considering the pressure Covid-19 has exerted on the sector. Still, being on the list is a testament to Chevron’s track record and stable dividend policy.

And even though the oil giant will probably not raise dividends this year, I believe it will not cut its dividend either. Chevron has made extensive cuts to its operational and capital expenses and with an unencumbered balance sheet, maintaining dividends will not be a major issue.

Chevron’s dividend yield is approximately 5.1% and that’s in no danger of falling due to its positive cash flow situation. The company is excellent in terms of cash flow generation and although revenues will take a hit this year, I expect it to be in a cash positive position sometime next year, as economies around the world shake off the financial impact of Covid-19.

Chevron Stock Valuation

On a trailing 12-month basis, CVX stock trades at a price-earnings ratio of 49.05 in comparison to an industry P/E of 11.05, as of this writing. The stock is an expensive one, with projections priced in. Despite that, I believe it still has a lot of upside.

Shares have dropped 15% in one year, so there’s still a lot of ground Chevron will make up. Revenue estimates indicate that 2021 is a year of recovery for the company and the wider sector. As demand for oil continues to rise as economies open up, valuations for companies like Chevron will tread higher as well.

Considering Chevron’s robust operational metrics, it won’t be surprising if the company emerges as an industry leader when the dust settles on Covid-19.

Final word on Chevron stock

Chevron management deserves a pat on the back for navigating the company through such troubled times. It’s never easy when you have such a fluid situation, but Chevron checks the boxes in several important categories. It has enough cash to survive the pandemic and credit agencies have affirmed its ratings, easing access to low-cost debt.

Moreover, the company has a strong and stable dividend policy due to its disciplined financial management. In a situation where many companies are looking to shed debt, Chevron can afford to take on more long-term obligations. Its high dividend yield is the icing on the cake.

Having said all this, it’s fair to say the stock is a bit expensive. But it still offers an attractive entry point.

I believe the stock has the legs to erase its losses and then some. Chevron stock is a buy for me.

Faizan Farooque is a contributing author for InvestorPlace.com and numerous other financial sites. He has several years of experience in analyzing the stock market and was a former data journalist at S&P Global Market Intelligence. His passion is to help the average investor make more informed decisions regarding their portfolio. Faizan does not directly own the securities mentioned above.