Earlier last week, Nvidia (NASDAQ:NVDA) briefly eclipsed Intel’s (NASDAQ:INTC) market capitalization of $260 billion. How could a company with 15% of Intel’s revenue and 13% of the operating income share the same market value? NVDA stock insiders didn’t care to ask. Since the end of March, insiders have unloaded over $97 million in shares, compared to $16 million over the same period last year.

When insiders sell shares that quickly, investors should ask themselves, “should I be doing the same thing?” With NVDA stock, investors would be wise to follow suit.

At $240, NVDA Stock Was a Buy. What About $405?

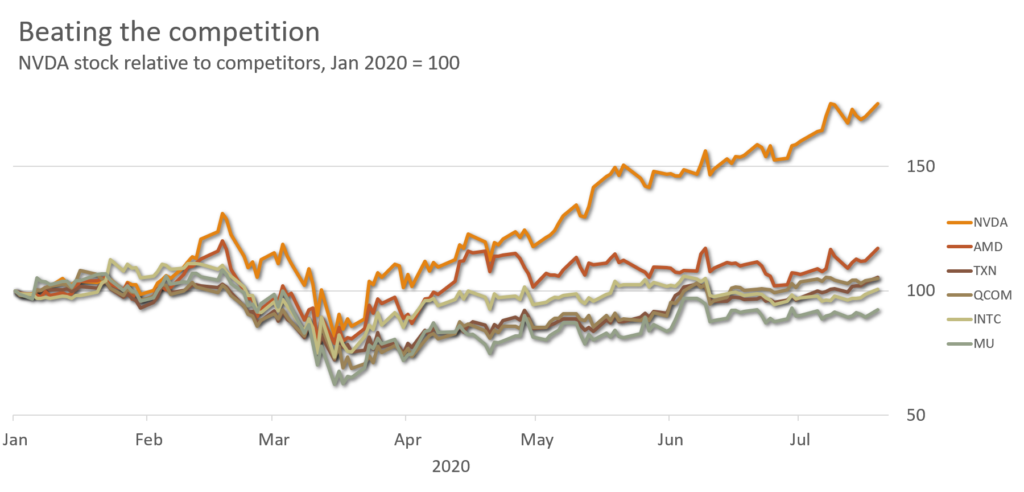

Nvidia’s shares have been on a tear this year. Between January 2020 through July, shares rose 70% from $240 as gaming video cards flew off virtual store shelves.

Nvidia is a leader in GPU processors. According to an independent report courtesy of Morningstar Research, Nvidia’s chips power almost 70% of all discreet GPUs, including those used in gaming and special AI applications.

Even Intel and Advanced Micro Devices (NASDAQ:AMD), the two behemoths in the semiconductor design industry, have struggled to compete with Nvidia’s lead in GPU processors. Analysts see further gains for NVDA, particularly in data centers and AI applications.

Insider Selling Often Predicts Bad News

Yet, these real-world successes haven’t stopped corporate insiders from unloading shares.

On July 1, Jen Sun Huang, the CEO of Nvidia, sold $38 million worth of shares in a single day. It was his first significant transaction in several years, and several other insiders followed suit.

On Wall Street, there are two types of insider trading. Firstly, there’s illegal type. Illegal insider trading happens when investors acquire and trade on nonpublic information. And there’s often billions to be made. There’s also a second type of insider trading: the legal variety. Legitimate insider trading happens when corporate insiders buy or sell shares in their own company.

How is this legal? Think of any employee who participate in Employee Stock Ownership Plans (ESOPs) or receives company stock options. They’re all insiders. And they all own shares.

Yet, corporate insiders often know far more about their company than the public does – from customer sentiment to internal financial reports. And their knowledge shows. Studies have shown that insiders perform far better than other investors: stocks that insiders sell drop an average of -5.5% within the next month. Over a year, stocks that insiders sell perform 6.88% worse than the market.

In 2Q18, Nvidia insiders sold $77 million of shares. NVDA stock finished the year down 42% after its soaring stock valuations fell back to earth. Will 2020 be different?

Nvidia Faces Some Uncertainty in Its Future

Despite rapid growth over the past 12 months, Nvidia’s fortunes have historically been volatile. Earnings per share rose from $1.08 in FY16 to $6.63 in FY19, before falling again to $4.52 in FY20. Revenues have also gyrated due to the changing demands of PC gaming and cryptocurrency mining.

Lumpy profits have made Nvidia a challenging company to forecast. On the one hand, analysts expect Nvidia’s revenue and EPS to almost double between 2020 and 2023. Intel’s revenues and EPS, on the other hand, are expected to rise just 15% and 29%, respectively.

Should NVDA Stock Holders Sell?

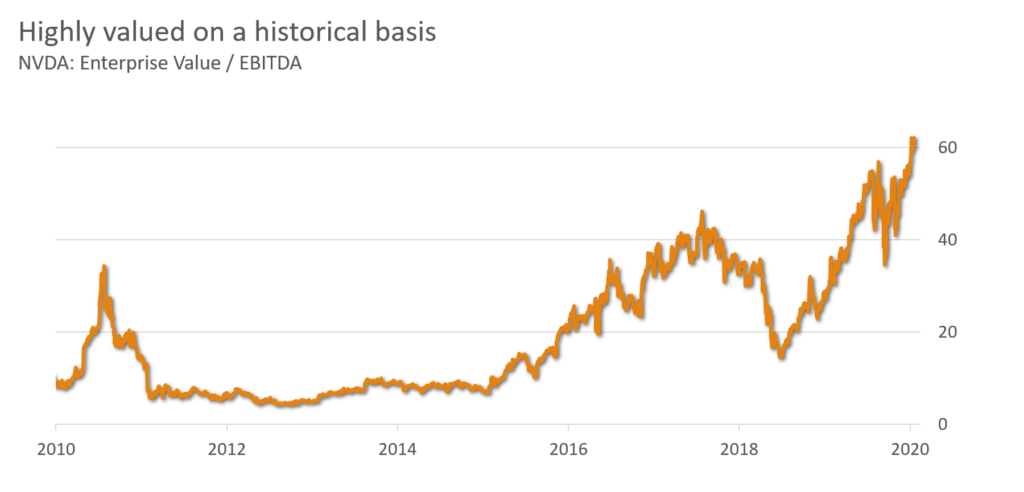

These lofty expectations for Nvidia’s future have boosted the company’s share price to a staggering 63x EV/EBITDA multiple, over four times its 20-year median of 14.6x EV/EBITDA.

Yet, doubling its sales in three years may prove difficult for Nvidia, given its saturation of the GPU market. The company would have to grow in data centers and automobiles, where it would start competing directly with Intel, a company with almost five times the R&D budget.

Some analysts have begun to sound the alarm. In a note to investors, Morgan Stanley analyst Joseph Moore warned about comparing Nvidia to high-growth software companies. “As much as we like the longer-term growth story, that’s simply not a comparison that we’re totally comfortable with,” he said in the letter. He continued to note that despite potential gains, share prices are “still a risk at current valuations.”

In other words, while prices *could* continue rising at Nvidia, corporate insiders aren’t taking their chances. And neither should regular investors.

Tom Yeung, CFA, is a registered investment advisor on a mission to bring simplicity to the world of investing. As of this writing, Thomas Yeung did not hold a position in any of the aforementioned securities.