AMD’s (AMD) shares are hovering close to their all-time highs but the rally could still continue. Latest data reveals that the chipmaker’s supply chain partners registered strong sales growth in October and November. This suggests that AMD is en route to posting a strong set of Q4 results which, consequently, can catapult its shares to new highs in the coming weeks. So, in my view, investors may be best served by holding on to their long positions in the name. Let’s take a closer look at it all.

(Image source)

The Data

I’d like to start by saying that AMD generally outsources most of its production, packaging and distribution of its CPUs and GPUs. The chipmaker designs its chips but they’re fabricated in foundries owned by Taiwan Semiconductor (NYSE:TSM) or GlobalFoundries.

These fabricated chips are then packaged together in the form of usable GPUs and shipped to end-customers by companies such as Gigabyte, MSI and ASUS. These firms also manufacture other products such as laptops (using Intel/AMD chips), PC peripherals (motherboards) and other networking gear. So, tracking the monthly sales figures for each of these channel partners can provide us with leading insights about how AMD’s ongoing quarter is coming along.

We at Business Quant have developed a tool which does exactly that, for over 1300 Taiwanese firms. The general rationale is that if these firms reported a sharp drop in their revenue growth figures in any month, then maybe AMD’s sales didn’t go so well for that particular month. Conversely, a sharp rise in their sales suggests that AMD is thriving as well and that the supply chain for PC parts is healthy and intact. Let’s now look at the sales data, below.

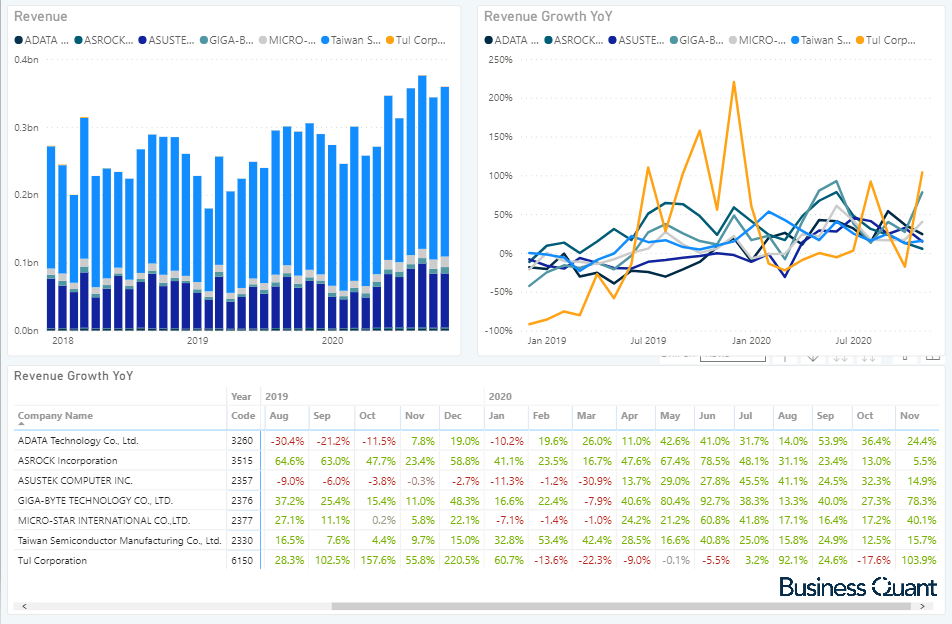

(Source: BusinessQuant.com)

As it turns out, all the firms saw their sales growing year over year during November. TUL Corp., which is an exclusive GPU partner for AMD, reported the largest sales increase in November. Other more diversified GPU and PC peripherals manufacturers such as Gigabyte, MSI, ASUS (OTC:AKCPF) and ASRock variably saw their sales grow in the last two months. AMD’s foundry partner, Taiwan Semiconductor, also saw a sharp surge in revenue growth in the mentioned time frame. This goes to highlight that AMD’s GPU and motherboard partners have been thriving of late. But what does this mean for AMD’s investors?

Why It Matters

I think it’s needless to say at this point but strong partner sales data is likely to result in strong sales for AMD. It’s very likely that these board partners registered breakneck revenue growth because there’s an unprecedented demand for AMD’s products. The chipmaker had recently released its new 6000-series GPU and 5000-series CPU line-ups which might have triggered an upgrade-spree amongst end-users and fueled this partner-wide sales growth.

The second thing worth noting here is that some of these partners reported a sales growth acceleration in October and November. Unless this was a one-time anomaly or was triggered by unrelated events, accelerating sales growth usually points to growing market traction or even market share. We’ll have to wait for official market share figures to come out but this sales acceleration does suggest that AMD is gaining market traction, possibly at the expense of its competitors (Nvidia (NASDAQ:NVDA) and/or Intel (NASDAQ:INTC)).

Next, AMD’s Q4 spans from October through December. These healthy channel partner sales numbers in two out of three months falling in the quarter suggest that AMD may very well be en route to posting a strong set of Q4 results and it might also go on to comfortably meet its management’s revenue guidance. For the record, the chipmaker’s management is projecting its Q4 revenue to come in at $3 billion, plus or minus $100 million.

Caveats

Having discussed the positives so far, I’d like to shift readers’ attention to some of the caveats of using this data. For starters, these vendors (except for TUL Corp.) don’t have an exclusive partnership with AMD. This means that we can’t rule out the possibility that their revenue growth in recent months was driven by products built for the Intel or Nvidia ecosystem while their sales of AMD-centric products stagnated.

I personally feel that’s not the case but I wanted to point out this caveat nonetheless. I believe so because all the vendors unanimously posted healthy revenue growth during October and November instead of just a few, which indicates that there’s an overall robust channel demand for AMD-centric parts.

Secondly, we can’t assume that these lofty revenue growth figures were driven by surging shipment volumes. We’ve seen retailers and resellers hiking their prices and capitalizing on the short CPU/GPU supplies in the last few weeks, so I contend that this transitory inflation may have played a role in lifting AMD’s channel-wide revenue figures higher.

Third, I would advise against jumping to conclusions. This channel partner sales figures are only until November whereas AMD’s Q4 spans from October through December. This means there’s still a month worth of channel data that we’re yet to factor for, before making any predictions or forecasts about AMD’s Q4 results. Although unlikely, a sharp drop in AMD’s partner-wide sales during December would raise new concerns and it might as well hurt AMD’s Q4 results. So, at best, we should use this data to have a general understanding that AMD’s Q4 is coming along strong.

Final Thoughts

If AMD’s products were out of favor, or out of stock, as the bears would lead us to believe, then we would have seen its partner sales declining in the months of October and November. But that did not happen. Instead, sales grew for all the board partners during November. This highlights that there’s a healthy global demand for PC parts, and especially for AMD parts. So, readers and investors may want to ignore the fear, uncertainty and doubt, and remain invested in the name. The chipmaker seems well poised to post a strong set of Q4 results and, as a result, its shares might rally further. Good Luck!

Author’s Note: I’ll be writing another article on AMD in the next two weeks, you can stay updated by clicking the “Follow” button at the top of this page. Thanks!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.