With its monopolistic position in the region e-commerce giant Jumia Technologies (NYSE:JMIA) is often referred to as the Amazon (NASDAQ:AMZN) of Africa. Jumia stock has seen a spectacular rise as a result.

When it first launched in 2012, its goal was to cement its position as the leading e-commerce player in the African continent.

Since then, it has firmly established its position at the top of the region’s e-commerce sector with its breadth of unique service offerings. However, Jumia’s stock price is completely out of touch with its fundamentals, growing by a whopping 676% this year.

Jumia has three primary segments, including its e-commerce marketplace, logistics, and its payment platform called Jumia Pay. It has broad regional coverage across the African continent, currently in its early stages of e-commerce and fintech penetration.

The company aims to offer its customers a one-stop solution to its customers, similar to its Asian and North American counterparts. Its asset-light model is helping Jumia in narrowing down its losses and move towards profitability. Despite these positives though, its financials do not justify its parabolic valuation at this stage.

Massive Potential for Expansion

Investors are jumping on Jumia’s hype train primarily because of the massive growth expected in e-commerce and fintech adoption in Africa. E-commerce and fintech are mostly untapped in the region, and with its fast-growing population, the opportunity is immense.

Its population will be growing at 2.7% per year, roughly doubling by 2050 to 2.5 billion people. Jumia’s primary market, Nigeria, is the third most populous country in the next 30 years.

Moreover, the region’s demographics will be dominated by the younger population leading to faster digitization acceptance. Research suggests that e-commerce will account for roughly 10% of the region’s overall sales by 2025. Therefore, its revenues of roughly $100 million are minuscule in comparison to its massive potential.

Additionally, an underbanked population in Africa presents a massive opportunity for Jumia Pay. A recent McKinsey report suggests that more than 60% of the continent’s population will have access to banking services by 2025. Hence, if Jumia makes the right moves and scales its offerings, it can establish its ascendency in the fintech world.

Valuation Isn’t Justified By Its Financials

At this time, the problem with Jumia is that its valuation is not in line with its financials. It recently posted its third-quarter results, which were essentially a mixed bag. Revenue was down 17.7% primarily due to its strategic shift towards an asset-light business.

Revenues from all three segments grew at a considerably slower pace than the same quarter last year. Gross merchandizing volumes also took a hit of roughly 28% year-over-year. Perhaps the star of its third-quarter was Jumia Pay, which grew by 50% with greater penetration rates. However, it is on the right path to achieve significant cost-efficiencies and move towards long-term profitability.

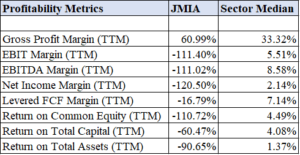

The tables above show the massive discrepancy between the company’s financial and price metrics to sector medians. From a financial standpoint, the company lags behind its competition by a fair margin apart from its gross profit margin.

Moreover, in terms of its price metrics, it is significantly overblown across all metrics than the sector median. Hence, I rest my case that its current valuation is completely unjustified at this time

The Bottom Line on Jumia Stock

Jumia has the potential of being the Amazon of Africa, but it’s not quite there yet. The company has the first movers’ advantage in the sector and has done well to expand its services in line with the growing African economy.

The potential of fintech and e-commerce is tremendous and has room for several players. However, Jumia stock is trading well over its mean price targets, and a significant pullback is imperative for investors to find it attractive.

On the date of publication, Muslim Farooque did not have (either directly or indirectly) any positions in the securities mentioned in this article.