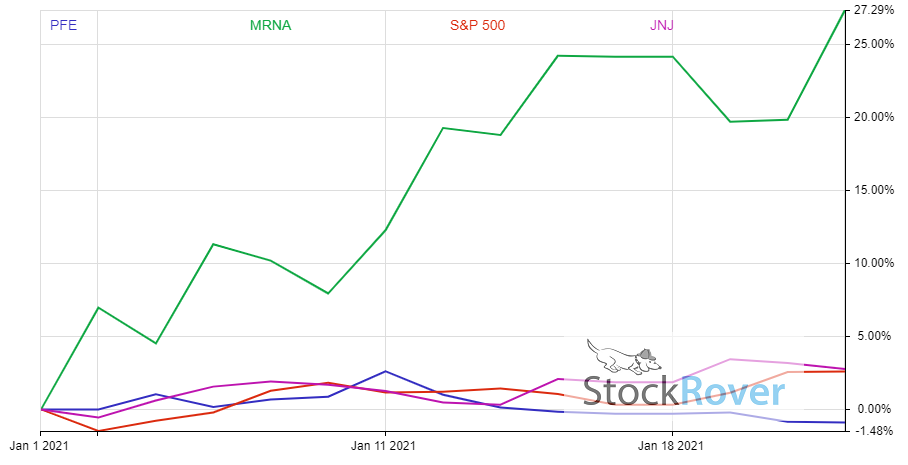

Pfizer (NYSE:PFE) stock is down nearly 1% so far this year. That’s strange, considering it got its vaccine out the door in record time. The novel coronavirus pandemic has wreaked havoc on the global economy. Pfizer and BioNTech’s (NASDAQ:BNTX) vaccine received Emergency Use Authorization (EUA) due to its excellent efficacy of 95%. But despite that, Pfizer stock hasn’t moved the needle.

That’s the part that confusing analysts. According to Morgan Stanley, Pfizer is projected to haul vaccine revenue worth $19 billion in 2021. And it’s expected to earn a further $9.3 billion in 2022. Despite all these positive catalysts, Pfizer stock is meandering along.

Retail traders are more attracted to electric vehicle (EV) stocks and SPAC plays. Solid performers are left in the dust as investors chase potential multi-baggers.

Despite a yield of 4.3% and 10 positive earnings surprises in the last 12 quarters, Pfizer stock continues to trade at 11.8x forward price-earnings. It has a 12-month price target of $41.8 per share, a 14.6% premium to the current price. No matter which way you look at it, shares are a bargain at the moment.

Pfizer Stock Is a Value Play in the Pharma Sector

Vaccine stocks are slowly losing steam after a bumper 2020. That’s because investors are booking their profits after valuations went supersonic.

However, we are still in the early days of recovery. The virus is surging, and initial vaccine supplies remain limited. The country’s immunization program focuses on the elderly and people with serious medical conditions, and essential workers. That means there are still millions of yet to be vaccinated.

Besides, the emergence of a new variant of the disease makes investors rethink the logic of abandoning pharmaceutical stocks quickly. The World Health Organization believes there is no impact on vaccines from the variant. BioNTech has also expressed confidence its vaccine is effective against the variant. However, the Pfizer and BioNTech partnership may still have to develop vaccines to deal with new strains of coronavirus. In such a situation, its research on Covid-19 will prove useful and reduce costs moving forward.

Amidst all this, Pfizer stock’s forward P/E is the cheapest among the major vaccine manufacturers. It’s expected to grow sales and EPS at 10.9% and 10.3%, respectively. Shares have a margin of safety of 27% and as I mentioned, seldom has a quarter gone by where the company hasn’t beaten Wall Street estimates soundly.

Come for the Valuation, Stay for the Dividend

Dividend investing is not something that you would associate with pharmaceutical stocks these days. However, having a sustainable income stream in addition to the growth in your portfolio’s market value from asset appreciation is important. It’s here that Pfizer gets top marks.

The company has hiked its distribution for more than 10 consecutive years. Considering the kind of sales growth the company is expected to see for the next couple of years, there is no danger it will cut its distribution any time soon, leading to a very healthy total return.

The only company with a close to 4.3% yield is AbbVie (NYSE:ABBV), with 4.7%. However, the Abbott Laboratories (NYSE:ABT) spin-off is not a frontrunner in the vaccine game, a major reason for investing in Pfizer stock.

Diversified Portfolio

Undoubtedly, Covid-19 associated vaccine sales are a major tailwind for Pfizer stock. However, the company also has other medical products that are doing well, especially its oncology portfolio, which contributes more than 10% to its overall top line.

For the past five years, revenues have grown at 32% due to Ibrance and Sutent’s success. Sutent is a $1 billion-plus drug, while Ibrance generates over $4 billion in annual sales. Additionally, Pfizer’s hemophilia drug candidate marstacimab is a major growth driver.

These have nothing to do with Covid-19 vaccine sales, which are expected to be a major driving force for the foreseeable future. Pfizer and BioNTech plan to produce 2 billion doses of their Covid-19 vaccine this year. Moderna (NASDAQ:MRNA), its closest competitor, does not have the resources to match Pfizer’s production capacity.

Attractively Placed

Unlike several of its peers, Pfizer stock hasn’t soared to dizzying heights. That says a lot of the speculative atmosphere that exists at the moment. People are investing less in established names. Instead, the focus has shifted to obscure companies in high growth niches.

Even if you feel that vaccine sales are a one-off, there is a possibility that future coronavirus strains could require new products. In addition, an attractive valuation, high dividend yield, and solid outlook make Pfizer stock a value play for me.

On the date of publication, Faizan Farooque did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Faizan Farooque is a contributing author for InvestorPlace.com and numerous other financial sites. Faizan has several years of experience analyzing the stock market and was a former data journalist at S&P Global Market Intelligence. His passion is to help the average investor make more informed decisions regarding their portfolio.