I’m officially in summer mode. The salty sea air. Ocean views. A love … of tech stocks. My hot vax summer is simple and breezy. But my relationship with Palantir (NYSE:PLTR) stock is a lot more complicated.

I’ve always had a very on again, off again relationship with PLTR stock. My current relationship status is off. Despite an established long-term bullish view on Big Data, I have two concerns with regards to Palantir.

First, the stock is expensive, trading at a premium to growth. Second, I think there is potential risk to the company’s forward estimates.

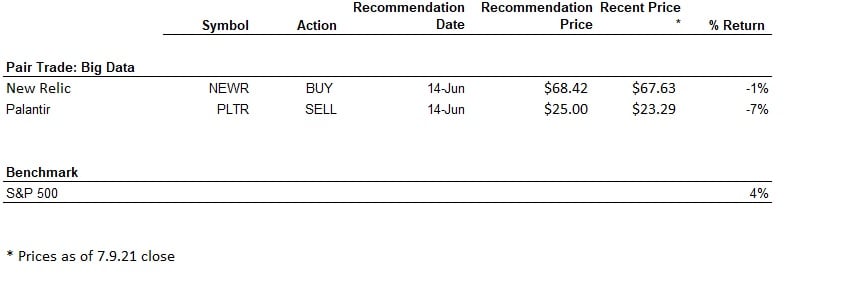

Since my June 14 sell recommendation on Palantir stock — part of my What to Buy, What to Sell series — PLTR shares have declined 7%. That’s modestly below the S&P 500, which has gained 4% over the same period.

PLTR shares are experiencing a correction. Why?

Simply put, growth investors have been trading with their emotions lately. They’re selling into PLTR’s recent strength. Since hitting a peak of $45 per share earlier this year, PLTR has fallen substantially and is now trading at round $25 per share. In fact, Cathie Wood’s ARK Next Generation Internet ETF (NYSEARCA:ARKW) sold more than 710,000 shares of PLTR stock. That’s its second sale in the data analytics company in the past few months.

If you’ve been as cautious on Palantir as me, you’re probably wondering if now’s a good time to buy. And if we’ve learned anything from the rise and fall of Workhorse (NASDAQ:WKHS) stock, it’s that Cathie’s loss can sometimes be investors’ gain. So, does the recent share weakness open up a good entry point in PLTR stock? Here’s a closer look.

PLTR Stock: An On Again, Off Again Trade

I really like Palantir stock — despite my lack of enthusiasm for special-purpose acquisition company (SPAC) IPOs. That says a lot for how spirited I am about Palantir’s unique technology edge and about the Big Data sector in general. Both are red-hot.

Investors have plenty of reasons to be bullish on Palantir’s long-term addressable market. Palantir’s Gotham software mines massive data sets for intelligence and law enforcement applications. Palantir is a certain beneficiary of the Biden administration’s heightened cybersecurity effort.

But despite showcasing strong healthy growth in its government business, there’s a flip side to PLTR stock. First, it has always been pricey (valuation still matters, even in a growth market). Second, there’s the lack of a real growth ‘spark’ in its enterprise business.

Here’s my quick take on the stock:

PLTR Investment Thesis

Pros:

- It’s in red-hot space with sustainable 30%+ revenue growth

- There’s a recent pullback in the stock

Cons:

- There’s potential for a broader sector correction

- We need more color on enterprise strategy to get comfortable with the long-term growth forecast

While I like Palantir’s long-term story and addressable market, valuation concerns have made this stock more of a short-term trade for me. But with PLTR stock trading around $25, down from $39 highs in January (and down roughly 7% in the past month), so, again, is now the time to buy? To answer that question, let’s see if anything significant has changed.

What’s Changed: Enterprise Strategy

I’ve talked about my issues with Palantir’s sales mix before. There’s no doubting the company’s incredible revenue growth in the government sector. The trouble is that things have been slow in the company’s commercial business. For those that aren’t aware, this segment represented 39% of Q1 sales. The company’s revenue guidance for 2021 to 2025 indicates consolidated growth of at least 30%. However, to reach this ambitious growth projection, Palantir needs to successfully alter its business strategy so that it gains more enterprise customers.

This enterprise shift is undeniably important for Palantir to be able to sustain its long-term growth rate. But things have been moving slowly. To accelerate growth, Palantir is doubling down on the healthcare side of its business. The company has made several big hires and announced marquee customers like the Food and Drug Administration, Centers for Disease Control and Prevention and National Institutes of Health.

Data privacy concerns run high in the enterprise market, and Palantir’s Foundry solution appears well-suited to address customer needs. Still, Palantir hasn’t reached good sustainable growth in the enterprise just yet.

What’s Changed: Valuation

This potential “mixed-bag” on long-term revenue growth is a good reason to revisit PLTR’s valuation. After a 7% pullback, PLTR stock trades at 30x forward sales. That’s in line with revenue growth.

Palantir’s valuation isn’t super exciting. But when it comes to the balance sheet, things look more attractive. With $2 billion in liquidity and the potential for a “home run” SPAC investment, Palantir becomes an even better fundamental story worthy of core-holding status. The company has participated in at least eight SPAC-related PIPE transactions, investing well over $100 million. These are a win-win for the company. Not only could Palantir win big from its investment stake in several pre-merger SPACs, it could also form a direct relationship that could lead to a partnership using its Foundry data analytics platform.

The Bottom Line on PLTR Stock

I like the healthy rationality that’s driving the correction in Palantir stock. While there are several potential upside catalysts, the stock looks fairly valued here. Near-term market turbulence is a good enough reason to exercise a bit more valuation discipline. As a result, I expect the shares to trade sideways as long as the company’s 30% growth rate continues. Despite the pullback, there’s still meaningful downside risk to PLTR stock without a strong enterprise ramp and a re-acceleration of growth.

If we wait this one out, we could see a more stable entry point in PLTR stock.

Your comments and feedback are always welcome. Let’s continue the discussion. Email me at [email protected].

On the date of publication, Joanna Makris did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Joanna Makris is a Market Analyst at InvestorPlace.com. A strategic thinker and fundamental public equity investor, Joanna leverages over 20 years of experience on Wall Street covering various segments of the Technology, Media, and Telecom sectors at several global investment banks, including Mizuho Securities and Canaccord Genuity.

Click here to track her top trades of the week, where she sheds light on market psychology and momentum, while leveraging her deep knowledge of fundamental analysis to deliver event-driven trading strategies.