U.S. home prices haven’t been the only thing skyrocketing during the pandemic.

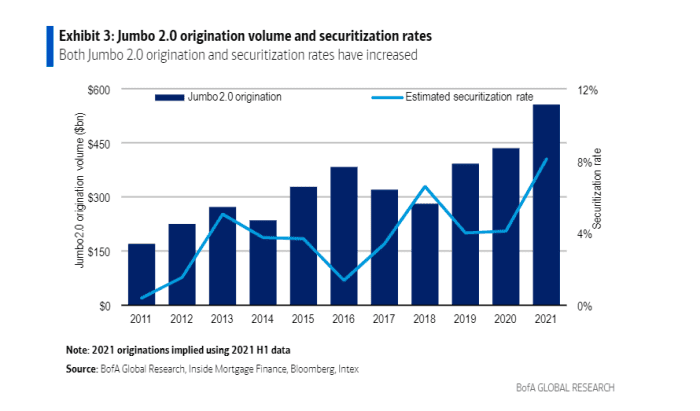

Originations of large “jumbo” U.S. residential mortgage loans that exceed “conforming limits” set for housing giants Freddie Mac and Fannie Mae could hit $550 billion this year, a level not seen since the run-up to the 2008 financial crisis, BofA researchers wrote Monday, in a weekly report.

They tallied jumbo originations at about $283 billion in the year’s first half, putting the annual volume within reach of a post-crisis record. With the surge, “a large share” has been held in bank portfolios, but an increasing slice also has been securitized, or packaged up and sold to investors as private mortgage-bond deals (see chart).

Jumbo home loan originations are surging.

BofA Global

Unlike the nearly $7.8 trillion agency mortgage-backed securities

MBB,

market, the riskier and much smaller $780 billion private-label sector, dominated in recent years by jumbo loans, lacks government guarantees.

Jumbo home loans mostly go to borrowers with prime credit scores who need financing above the conforming limit set out for housing giants Freddie Mac

FMCC,

and Fannie Mae

FNMA,

That’s currently about $548,000 on single-family residences in much of the U.S., but closer to $820,000 per home in New York, San Francisco and other high-cost areas. Those levels can increase annually.

Several public mortgage lenders, including PennyMac

PFSI,

in recent weeks have said they would offer borrowers confirming loans of up to $625,000, a level that’s anticipated to match the new federal guidelines for 2022, which are expected to be announced in November.

The race to make large loans on expensive homes comes as property prices have surged during the pandemic, up almost 20% from a year ago, as of July, while touching fresh records in many cities across the nation.

Jumbo mortgage-bond issuance this year has already hit a post-2008 record of $38 billion, with $45 billion likely by year’s end, according to the BofA team, which noted an expanded investor base for private-label mortgage bonds, but also low credit losses and “strong” origination guidelines.

It has been about 15 years since Wall Street fueled a boom in high-leverage mortgages to risky borrowers and a suite of exotic, housing-related derivatives that imploded when home prices tumbled, taking down investment bank Lehman Brothers and prompting a wave of U.S. and European bank bailouts.

Since that time, big banks have been required by regulators to hold more capital against potential loan losses, but also briefly during the pandemic were temporarily prevented from buying back their own shares.

Investors will be waiting to hear more about credit conditions from top executives at JPMorgan Chase & Co.

JPM,

Bank of America Corp.

BAC,

and Citigroup Inc.

C,

when they kick off quarterly earnings this week.

Credit in the American housing market has expanded, but remains relatively tight in the years since millions of U.S. homes ended up in foreclosure. Qualified borrowers recently could get rates on 30-year fixed home loans below 3%, a cost-saving offset to the affordability crisis faced by many looking for a starter home.

Wall Street largely expects the Federal Reserve to spell out its plan in November for tapering its $120 billion in monthly emergency purchases of Treasury and agency mortgage-backed securities, a way of pulling back its monetary largess as the U.S. economy heals.

Signs that higher longer-term borrowing costs could be afoot for the U.S. economy can be traced to the 10-year Treasury rate’s

TMUBMUSD10Y,

recent climb to 1.6%, it highest level since June, according to Dow Jones Market Data.