There are very few optimistic investment experts out there, so let me brighten up your day. I still believe that the indices can make new highs this year. The fight between the buyers and sellers now is uneven. The bears have a slew of tailwinds and they still can’t kill this bull. Wednesday markets rose 3% going into a potentially disastrous inflation report today. Last week the S&P 500 and the Dow were flat in spite of the war fears. Therefore, I should continue to find bargain stocks among the rubble of this correction. Today we debate three restaurant stocks to buy, which offer compelling scenarios.

I am optimistic but reckless. Nothing I do with stocks now comes with complete conviction. The issues plaguing the world are incredibly serious and investors must respect that fact. So when I initiate new risk it should be a starter position at most. And I would avoid adding to current positions because averaging down only makes problems bigger. Doing so when we have no new information about the risks is silly.

The largest threat to stocks is a threat to humans, too. The situation in Ukraine continues. World leaders are trying to compel Russia to stop its offense. But so far, the pressure has failed to dissuade them. Until that happens, the equity markets are at risk from disaster headlines.

Another nagging issue comes from the Federal Reserve. They have announced their intentions to end the quantitative easing this month and start raising rates. This is to combat inflation, which clearly is on fire. For over a year they told us that it was “transitory” and apparently now it is panic-worthy.

I bet that they won’t hikes as many times as experts are predicting. Nevertheless, the threat of extra tight monetary conditions persists. Meanwhile, we continue doing homework to find stocks at bargain prices.

Here are today’s three restaurant stocks to buy this month:

Restaurant Stocks to Buy: McDonald’s (MCD)

The invasion of Ukraine is devastating to the people who live there. Western governments are threatening consequences to Russia if they don’t back out. Corporations are too. Yesterday we learned that McDonald’s and Coke (NYSE:KO) are cutting off Russia from their products and services. This is the kind of fighting I prefer to one that actually costs human lives.

While this caused MCD stock to fall, it is doing so into prior support levels. Approaching $220 per share, more investors should become interested in owning it. The support zone extends another $20 lower, so it’s not a hard line in the sand.

Nevertheless, it is now both a fundamentally and technically compelling bullish argument for the long term. Since we do have so many extrinsic factors, however, investors should only take partial positions to begin.

Arguably, this stock debacle started Feb. 24. When MCD lost its support, the downside target has been a self-fulfilling prophecy. While markets bounced that day, MCD stock triggered a bearish head and shoulders bearish that targeted $225. Sure enough, what followed was exactly a correction to that destination.

The downfall was pretty severe and it cut through a lot of support. I would have expected more buyers showing up around $230 per share. However, these are unusual times so there are no guarantees.

Fundamentally, there’s nothing wrong with MCD except for temporary disruptions. The impact estimate of the Russia step is around 5% on its financials, so it is not an insurmountable challenge. The company has been around for ages, and I’m confident they will navigate the hot waters well. Especially since they actually planned their actions and they are in the driver’s seat.

The company’s profit-and-loss statement is somewhat boring but that’s the selling point. There isn’t a financial cliff they’ve stepped over to cause this correction. Moreover, it is not expensive, so boring financials mean the absence of special bearish circumstances.

They generate $9 billion in cash from operations, so they can survive this Russian situation. Meanwhile, MCD almost 20% below its highs is worth investigating, especially for new positions. I am not a fan of averaging down unless the initial position was partial to start.

Chipotle (CMG)

Within the restaurant industry, Chipotle is the tech forward one to chase. If McDonald’s is the Apple (NASDAQ:AAPL) of restaurants, then CMG is the Amazon (NASDAQ:AMZN) of the group.

I’ve analyzed restaurant financials for a long time and what CMG does is absolutely incredible. For a long time they have drawn criticism for their valuation. However, usually they’ve earned it by delivering stellar comps. That’s why the stock is so volatile because it has extreme fans and haters at odds. Each group makes solid arguments, but somewhere in the middle lies the truth. Management has earned all the kudos it needs to attract buyers of a stock on dips.

Recently, Chipotle stock has fallen onto hard times. After hitting an all-time high last September, CMG stock lost up to 35% of its value. This is where it will find support but with a giant caveat of risk. If it falls below this week’s low, it could trigger another giant drop below $1,000 per share. While that is not my forecast, it is too close to current price to ignore. Therefore, suggesting bullish positions here must come with two warnings.

The first is to take only partial positions leaving room to add in case the crash happens. Second is setting a stop loss so to make this entry more tactical than tech fundamental. The reason I fear the support below is because the downside target would become a self-fulfilling prophecy. We saw it happen to MCD, so the trading algos chase it here too. This would also be a bearish head and shoulder pattern and they are pretty reliable.

Fundamentally, there is absolutely nothing wrong with the company. Revenues now are almost 60% larger than five years ago. Moreover, management is now operating with a $650 net income line item. Statistically, this stock has never been cheap, but at this stage it’s not expensive either.

For a growth company, having a 57 price to earnings ratio is not that strange. This is especially true if the price to sales ratio is under 5. Owners of CMG stock here are realistic with their expectations. It’s important to also note that Chipotle has a $1.5 billion net operating cash flow from its own operations. So, they have all the ammunition they need to pursue growth even as borrowing costs rise from rate hikes.

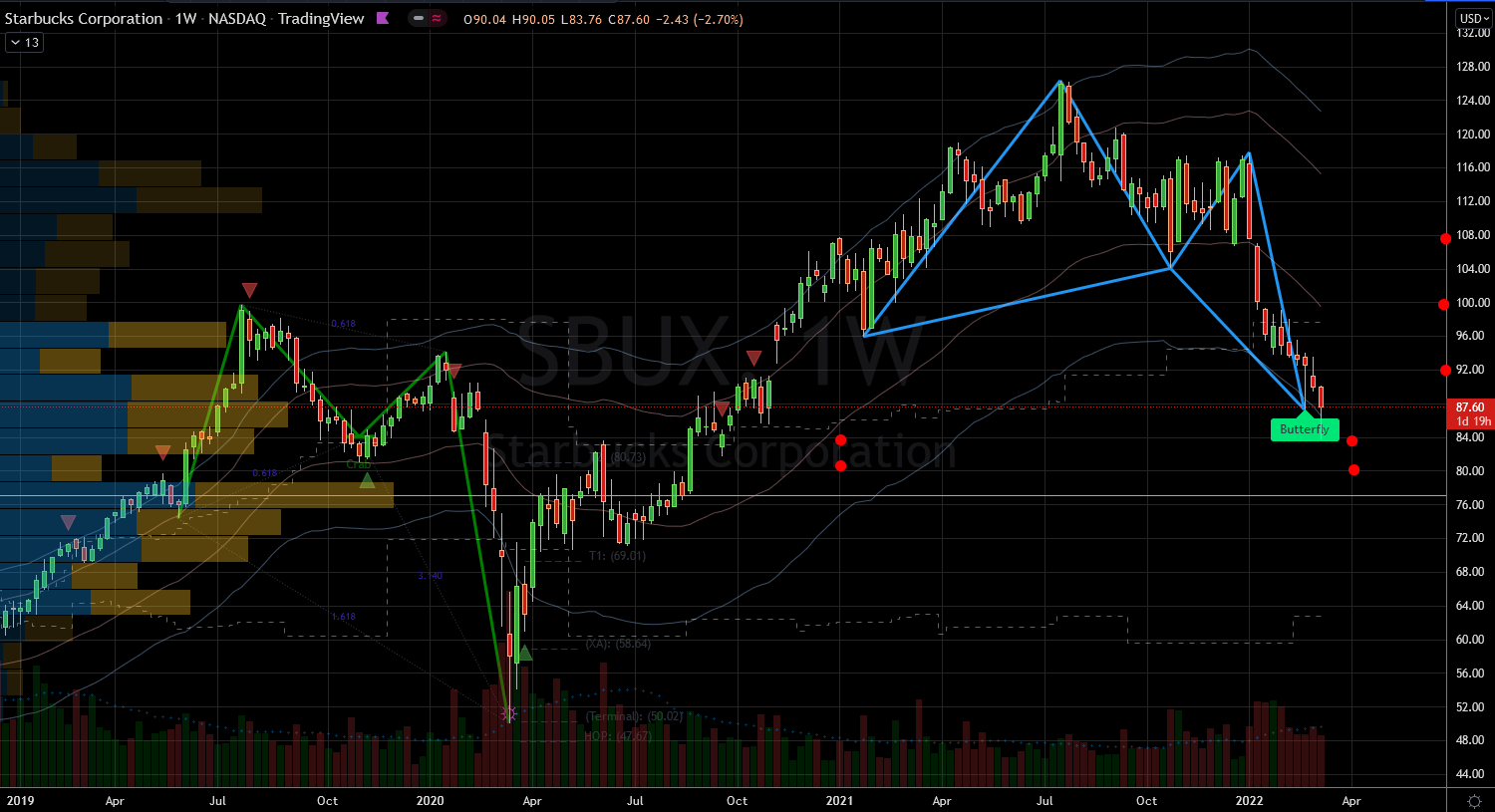

Restaurant Stocks to Buy: Starbucks (SBUX)

Starbucks stock is also hurting down more than 30% since its July highs. This one has also reached a level that should draw out perspective buyers. There is technical support for SBUX stock below $84 per share.

Since the fall from grace has been so fast, investors should not expect a hard line bounce. Think of it as a cushion, so it can still fall further. Coming down from the top to here was easy. However, falling much further from here will be more difficult. This company rarely makes mistakes and when they do they correct them quickly. Therefore, if the stock market stabilizes then I expect a rebound from SBUX.

The bulls need to know that the sellers are in charge until there’s evidence otherwise. Step one for them this week and next is to hold above $84 per share. Otherwise I expect the selling can continue for another 5% lower. The rebound rally can happen over the next two months, and it will face resistance. There will be sellers lurking if they can reach $96 per share. More of the same will be near $105 per share.

Bullish investors also need to realize that the upside potential is not da moon. I would be a fan of selling bull put options spreads to generate income. These are strategies that do not need rallies to win, and they leave room for error.

SBUX equity buyers should consider deploying only partial positions and staying tactical. Meaning I would be ready to book profits much faster than normal. The days of buy-and-hold are in the past and everyone needs to be a bit of a trader now.

SBUX also generates a lot of cash from ops, so financing is not an issue in a rising rate environment. Unlike McDonald’s, its P&L is not boring. Starbucks revenues are now 24% larger than 2018. They even clear $4.4 billion in net income. This management team is doing things right and overcoming challenges.

The pandemic shutdown for all three companies was as tough a test as you could ever deliver. All three passed with flying colors.

On the date of publication, Nicolas Chahine did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.