[Editor’s note: “Fears of a Housing Market Crash Are Creating Huge Opportunities” was previously published in September 2022. It has since been updated to include the most relevant information available.]

Everyone’s worried about a housing market crash. But data strongly suggests that those fears are grossly overexaggerated. And they’re creating some extraordinary investment opportunities with massive upside potential.

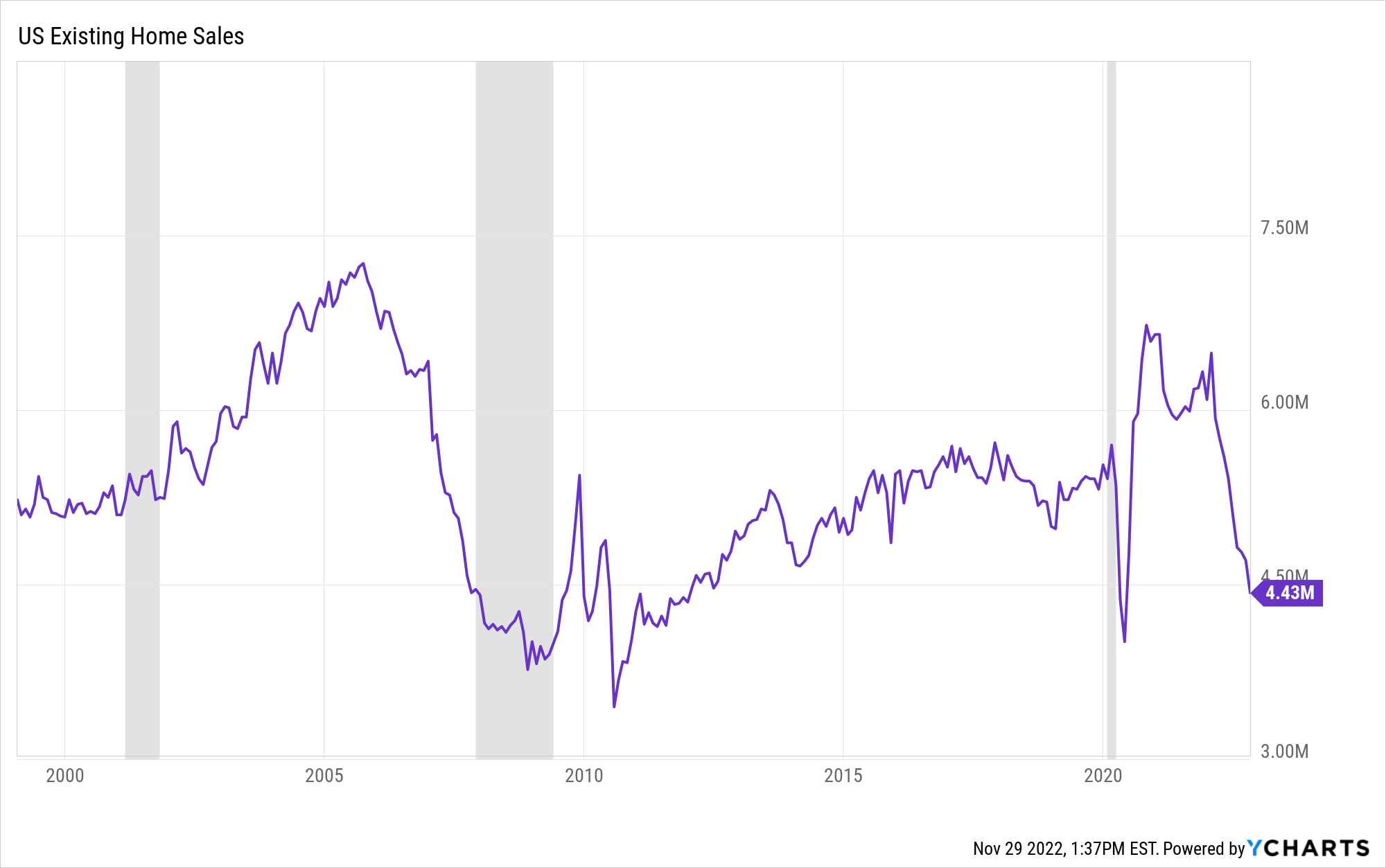

It’s quite easy to see why folks think a housing market crash is just around the corner. Home prices surged during the pandemic to unfathomable levels. But due to ultra-low mortgage rates, those home prices were still quasi-affordable. But now those mortgage rates have been spiking, and home affordability is crashing. As a result, lots of buyers have backed out of the market. You’re seeing price cuts on homes for sale, and existing home sales are dropping.

This is certainly starting to feel like the beginnings of a housing market crash.

But it’s not — far from it.

Talking heads are saying the housing market is about to crash like it’s 2008 all over again. But what we’re seeing today is the farthest thing from a 2008 repeat.

Instead, the market is normalizing, not crashing. And it’ll sustain healthy growth trends over the next few years. In fact, we talked all about these housing market movements in a recent episode of Hypergrowth Investing.

The opportunity? Wall Street has given into these fears of a housing market crash. And it’s left certain housing-related stocks trading at absurdly cheap valuations. Once time proves that these crash fears are baseless, those stocks will fly higher.

We’re talking potential 2X, 3X, even 5X gains in certain housing-related stocks in less than 12 months. And we’re confident in that call.

Here’s why.

Supply and Demand Fundamentals

At the end of the day, what drives the price of any asset? Supply and demand.

Low asset supply coupled with its high demand leads to that asset’s high prices. Conversely, high supply coupled with low demand leads to that asset’s low prices.

The housing market is no different. When home supply is low and demand is high, home prices go up. When home supply is high and demand is low, home prices go down.

Normally, the supply-demand fundamentals in the housing market are pretty balanced. Demand is durable because the desire to own a home is fairly steady over time. Supply fluctuates but normally within a well-defined range. The result — home prices almost always go up.

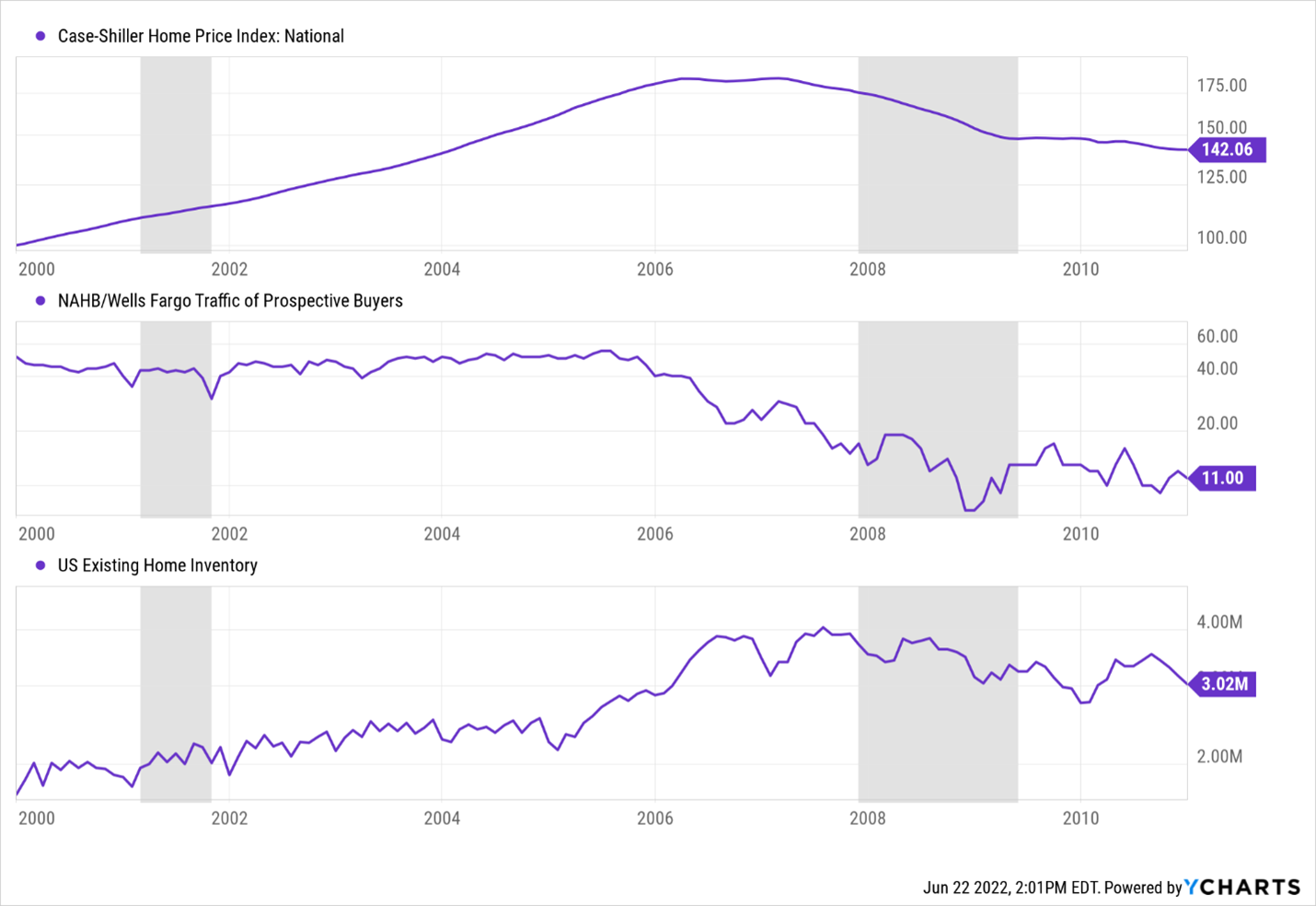

There are rare exceptions, and 2008 was the largest of them all. In that year, you had a confluence of unusually high supply converging on unusually low demand. And that resulted in the largest housing market crash in U.S. history.

But that was an exceptionally rare occurrence. Indeed, it takes a lot to move home prices down. You need demand to fall out and supply to boom, which almost never happens.

It did happen in 2008. But it’s not happening in 2022. And the fact that it’s not is creating some big buying opportunities.

Demand in the Housing Market Is Still Strong

A lot of folks are concerned about the falling demand for homes. But we think those concerns are still premature.

When it comes to demand, there are two inputs — desire and ability. Do people want to buy a house? Can they afford to?

Now, recent data does show that both inputs are showing signs of weakness.

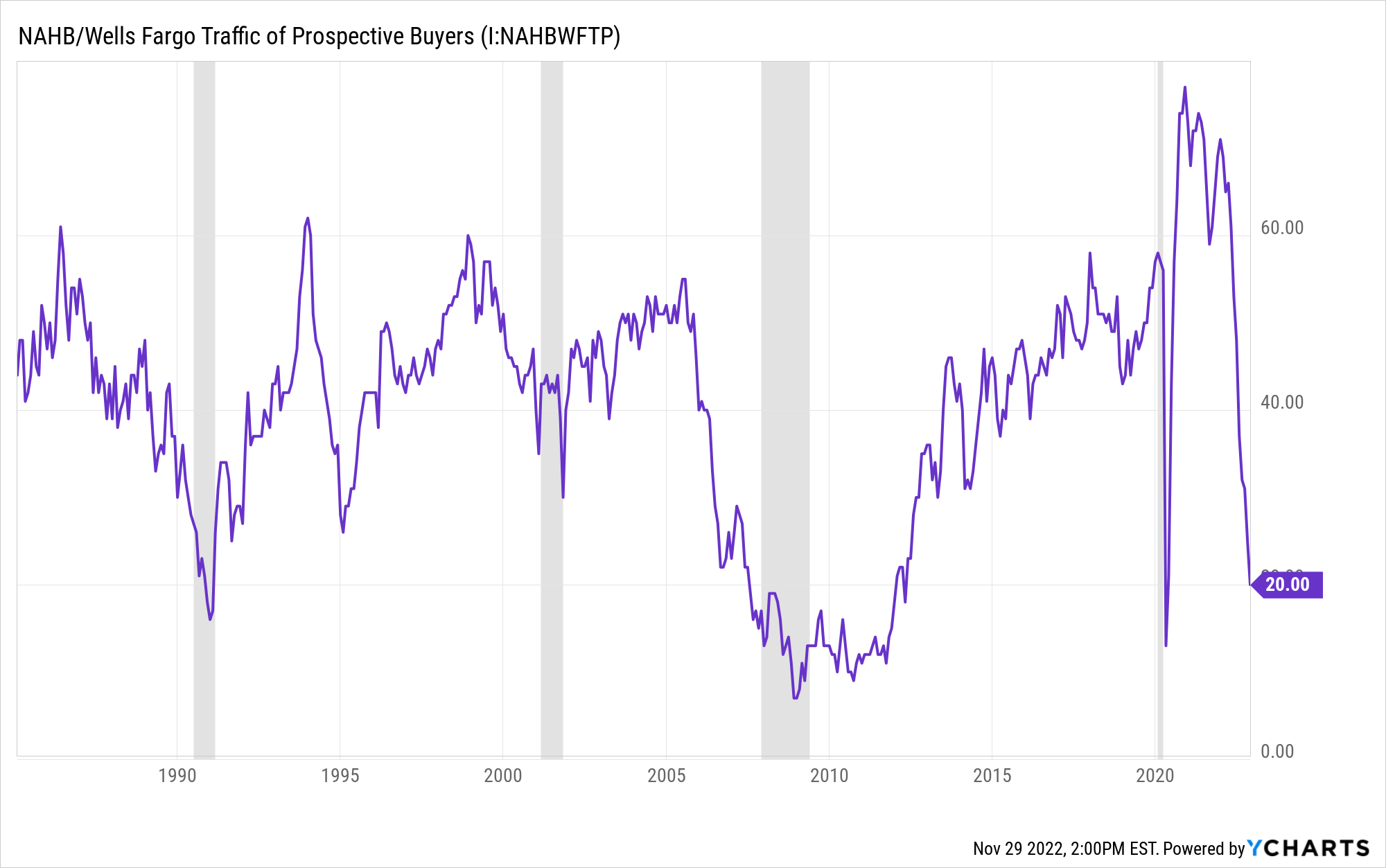

The NAHB index for the traffic of prospective buyers is probably the best metric for gauging home-buying desire. It measures buyer traffic in the housing market in any given month. If folks are going to see homes, they’re likely interested in buying one.

That index currently stands at 20. That’s down from where it was throughout 2021 (above 60). But it’s also above where it was when home prices started to decline in the early 1990s and the late 2000s (sub-20 readings).

The desire to buy a home is still above where it was during previous periods of home price declines.

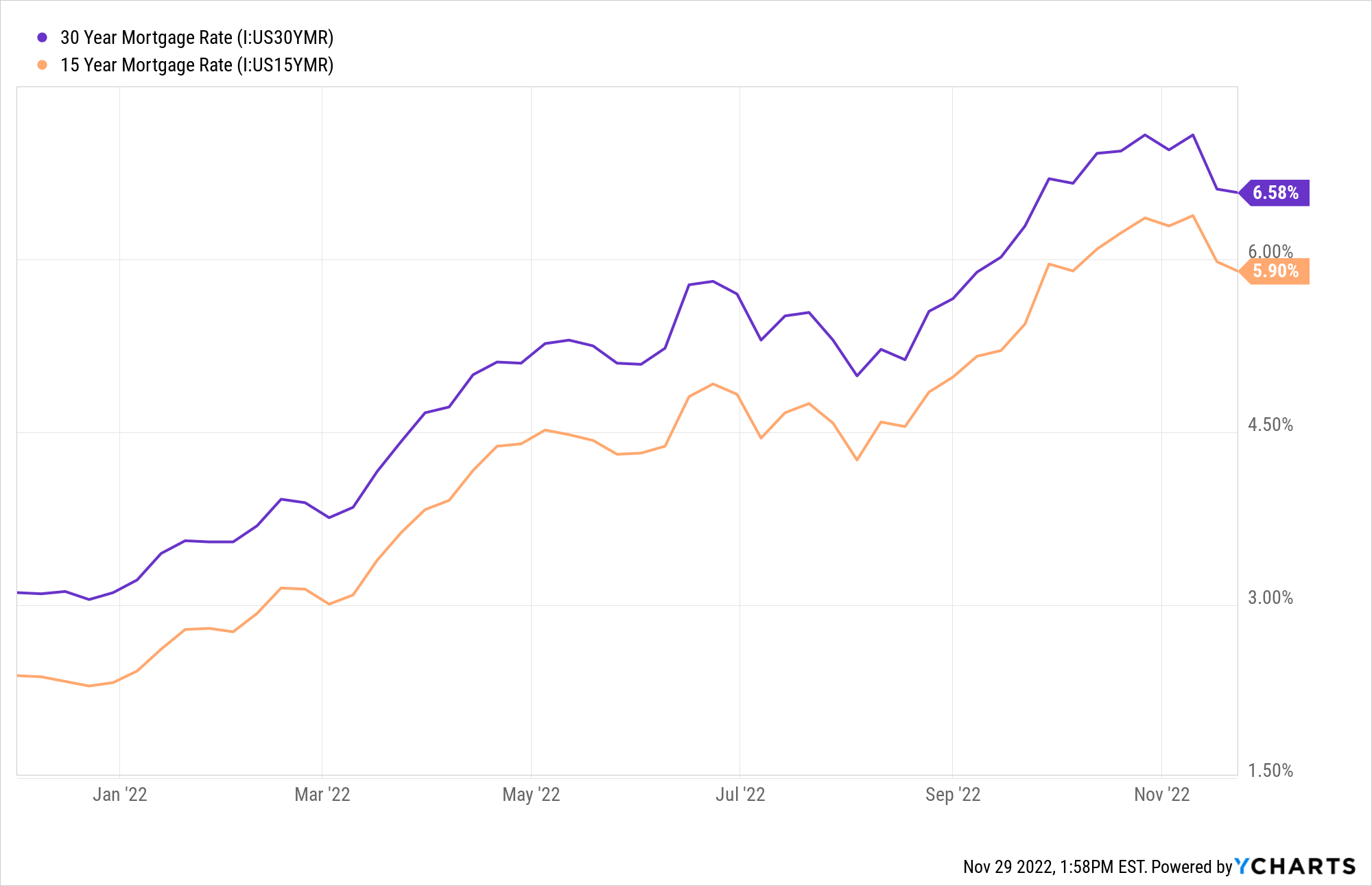

What about affordability? It’s crashing, yes.

The U.S. Fixed Housing Affordability Index currently sits at 96.6. It’s within the realm of the sub-100 readings we had during the two previous eras of home price declines.

However, so long as mortgage rates don’t keep spiking, the current level of affordability is sustainable. And given the Fed’s likely path forward, it’s entirely possible that rates have peaked.

As you can see in the chart above, mortgage rates have been on the decline recently. And we think that trend may just continue.

Inflationary data points to a smaller-than-expected rate hike of just 50 basis points in the month of December. The Fed has been hiking aggressively by 75 bps all year long. That’s quite a favorable development for the path of mortgage rates.

Not to mention, the data also points to a dovish evolution of the Fed in the near future. We could see a pause in hikes by early 2023, even cuts by the middle of next year. If that comes to be, mortgage rates will only continue to decline from here. And affordability will start coming back to life.

So, don’t despair just yet. As long as mortgage rates stabilize, housing market demand will remain healthy for the foreseeable future.

And that’s very bullish for housing-related stocks.

Supply Is Very Low

The reason we’re so confident in our call that the housing market is not crashing has to do with supply.

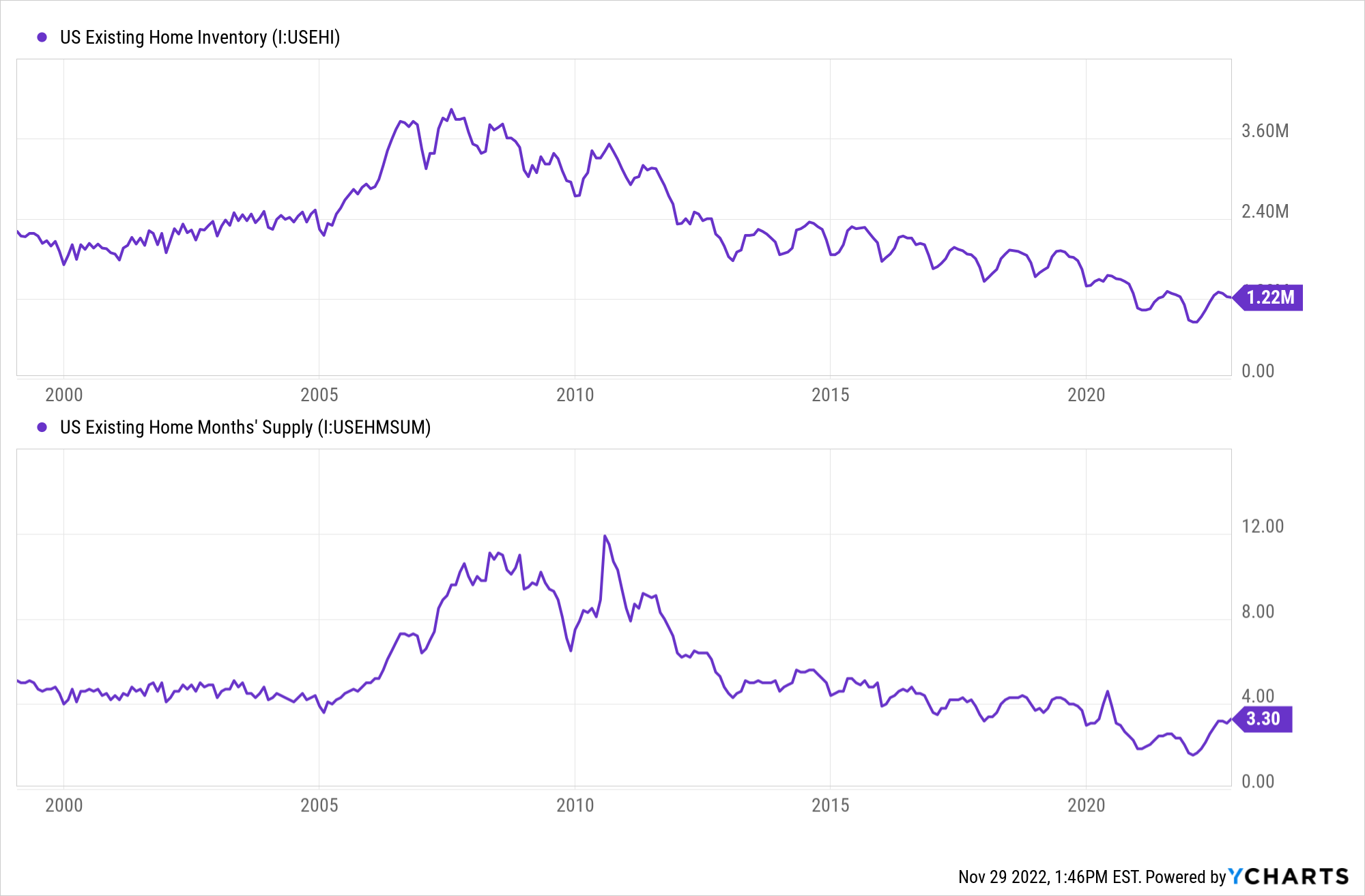

We’re currently in the most under-supplied housing market in history.

There are presently 1.2 million homes for sale in the U.S. housing market. That means that at current buying rates, it would take about 3 months to clear the entire supply (months’ supply).

Those are abysmally low numbers.

For example, when home prices started to go flat in 2005, housing inventory numbered about 3 million homes. And months’ supply clocked in around five months. Home prices didn’t start to decline until 2007. That’s when inventory shot up to 4 million homes, and months’ supply ballooned to 10 months.

In short, the last time home prices declined, the housing market supply was about 4X bigger than it is today. We had 4X the number of homes for sale on the market. And it took 4X longer to clear all those homes than it does today.

With supply this low and demand still pretty robust, it’s hard to see how home prices could take a big hit. Could they fall? Yes, but not by much. There’s simply too much demand chasing too few homes to warrant a big price drop.

In the absence of a big price drop, certain housing stocks look like multi-bagger opportunities at the current moment.

The Final Word on the Housing Market

Home prices don’t always go up.

But since 1960, they’ve gone up on a year-over-year basis about 90% of the time. And when they go down, they barely drop, with an average year-over-year decline of less than 4%.

In other words, home prices rarely go down. And when they do, it’s not by much. To see a repeat of the 2008 crash, you’d need a lot of external forces to create that situation.

We simply don’t have those forces today.

We’re in the most under-supplied U.S. housing market in history with still-decent demand. That’s a combination that’s far from extreme enough.

So… what will happen to home prices over the next few years?

Home price growth will moderate significantly. Currently, prices are rising by about 15% year-over-year. Since 1960, the average annual home price growth rate has been around 5%. We think we undershoot that for a few quarters and fall to 0% to 2% growth until affordability increases. Then, we’ll get right back to that historically normal 5% growth rate.

Expect a housing market slowdown over the next 12 months, followed by a resumption of historically normal growth trends.

We’re staring at a normalization — not a crash.

There is a silver lining to these pessimistic fears, though. Certain housing-related stocks are priced for a crash. They’re trading like its 2008 all over again, but it’s not. And once the market figures that out, these undervalued housing stocks will soar!

We have the No. 1 stock to buy for this housing market resurgence over the next 12 months.

It’s the most undervalued housing stock in the market today. It has more growth firepower than all the other housing stocks put together. And it holds so much long-term potential that it’ll make your jaw drop.

This is a stock that you simply need to hear about today — if you’re serious about making big money in the markets, that is.

Learn more about this moneymaker.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.