Shares of AMC Entertainment (NYSE:AMC) surged 23% on Monday after a Delaware court announced it would delay the conversion of APE units into common stock. The theater chain is now barred from amending its certificate of incorporation until at least April 27.

These moves have obviously frustrated arbitrage traders. Share conversions are a normal course of business, and the APE/AMC spread should have theoretically vanished by March 14 if things went to plan. Corporate boards prefer meetings to look like weddings, where the right people are coached to say “I do” at the right time.

But this is the real world, a place where couples get cold feet and wedding chapels catch on fire. AMC shareholders seem to be gearing up for a messy legal battle, which could delay or entirely derail the APE deal. The convergence trade also involves short-selling AMC, a move that should make most hedge funds think twice. In the past fortnight alone, an unhedged short AMC position would have lost 75%.

Still, the widening gap between AMC and APE shares should eventually make the gamble worth the risk. And if you’re willing to take on more risk than the average arbitrage trader, then APE shares are becoming an enormous convergence trade… with a rather large wrinkle.

What Is the AMC/APE Convergence Trade?

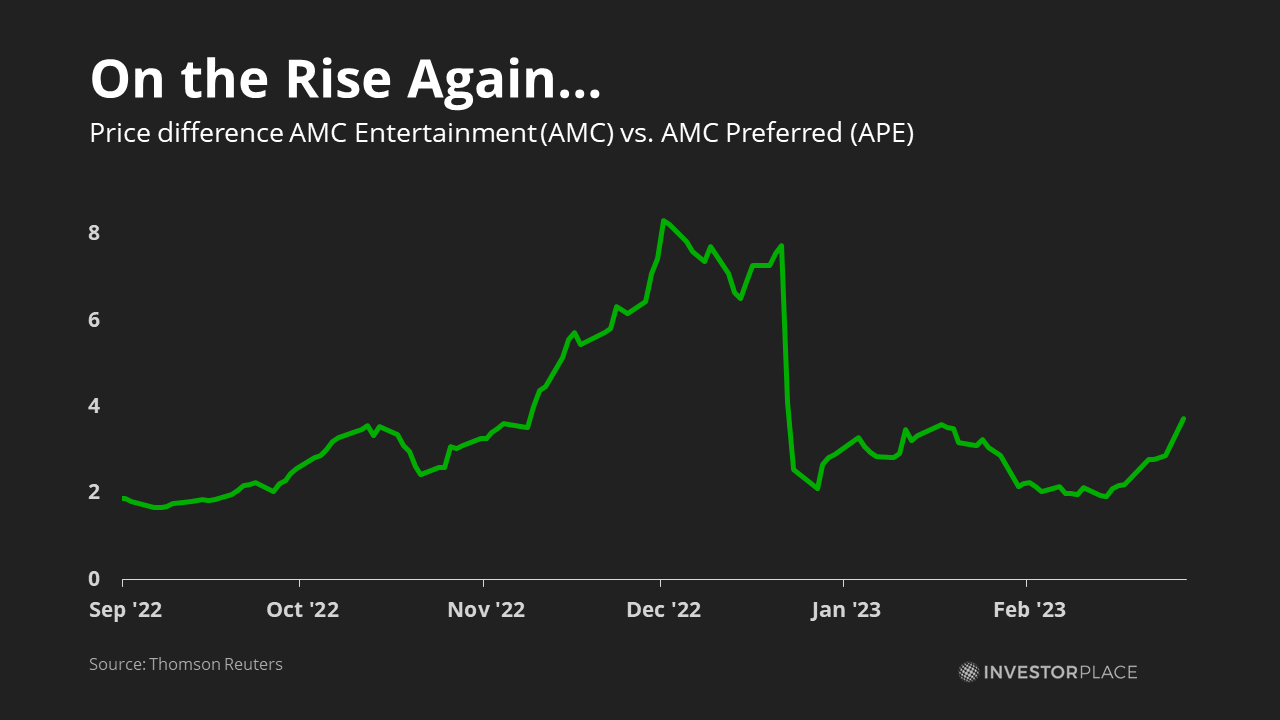

The AMC/APE convergence trade essentially involves buying the lower-cost APE shares and shorting the higher-cost AMC ones. If management successfully converts the newer APE shares into the regular AMC version, traders walk away with a profit per share equal to the initial spread. In our case, that’s $8 – $1.80 = $6.20. It’s a form of arbitrage that has existed for decades, although usually with a far smaller gap.

There are, however, some issues with this arrangement. First, AMC’s stock is highly shorted, making hedging essential. Buying offsetting calls, known as “delta hedging,” would cost around $1.80 per share through July 2023, or $2.25 through January 2025. That would eat into potential returns, making the arbitrage opportunity less attractive.

Second, AMC’s low float makes the shares extremely expensive to short. Fee rates are as high as 200% per year, meaning it could cost as much as $5.30 to sustain the position through the end of Q2. If the APE conversion gets delayed beyond that point, the convergence trade collapses and arbitragers walk away with nothing.

And finally, synthetic convergence trade strategies are unattractive, thanks to AMC’s inflated price. July’s at-the-market put options cost around $4.50, and May ones are little better.

That means there’s only one clear way to profit from this gap:

Buy preferred APE shares and ignore the AMC common issue.

The Origins of the APE Trade

In August 2022, CEO Adam Aron hatched a cunning plan to raise more capital. By issuing shiny new preferred APE shares (rather than the dull AMC type), the theater chain’s boss could side-step the 524 million AMC share cap and generate a ton of cash from willing retail investors.

It was a win-win for the firm and its stakeholders. Retail investors could continue ignoring management’s pleas to vote for a share increase. (The Reddit crowd, after all, is notoriously poor at showing up for proxy meetings). And Mr. Aron could use APE’s proceeds to chip away at his company’s enormous $5.3 billion debt pile. Without that financial lifeline, AMC would be out of cash within 3-4 quarters.

This unspoken truce is now coming to a head. On Jan. 27, AMC announced plans to convert APE shares into ordinary AMC ones, turning its “unofficial” capital raise into a decidedly official one. The March 14 vote is all but guaranteed to approve the APE-to-AMC conversion since APE voting power now trumps AMC’s by a 1.25-to-1 ratio. Prearranged agreements with hedge fund Antara Capital and Computershare Trust further stack the chances in favor of conversion. Meanwhile, AMC shareholders have revolted, with one class-action suit calling Mr. Aron’s APE shares “an exercise in 3-D chess” that would “eviscerate” common stockholders.

This opens up an intriguing opportunity. With APE shares now trading for a tiny fraction of AMC ones, something will eventually have to give.

How About a Game of 3D Chess…

APE shares have consistently traded at a significant discount because of their unclear standing.

On the APE’s side of the argument, Aron issued the preferred shares following the letter of the law. AMC’s registration state of Delaware has no clear limitations on preferred share voting rights, so issuing voting APE shares is perfectly legal in the state. Mr. Aron also had limited options in fundraising during the 2020 Covid-19 pandemic. If he failed to create the new share class, AMC would likely have folded the same way as Regal Cinema parent Cineworld (OTCMKTS:CNNWQ) did this year. And if that argument fails to impress the judge, the defense can point to the firm’s corporate governance guidelines, which prioritize the “long-term health and overall success of the business,” not shareholder voting rights.

On the other hand, the intent of Mr. Aron’s deal is more questionable. Regulators largely frown on the unilateral dilution of voting shares, which is why most preferred stock are issued with zero voting rights. Through this lens, AMC’s issuance of 642 million APE shares went against shareholder interest; management could have easily issued non-voting preferred stock. AMC’s management also never gave common shareholders a chance to reject the dilutive issuance. In July 2021, the firm withdrew its proposal to add 25 million shares to its count before a vote could happen.

That’s created a mess worthy of a Star Trek reference to 3D chess.

…Or Maybe Checkers Instead?

Arbitrage traders have history on their side. Around two-thirds of all shareholder lawsuits regarding fiduciary duty are dismissed, and much of the remainder are resolved through settlement. The APE/AMC gap is also startlingly large. Even if we assign a 25% chance that APE shares go to zero, our expected delta-hedged return remains well above 50%… if only the courts toss the injunction by April 27.

But such fancy footwork adds a great deal of risk. The courts could easily delay the APE/AMC conversion, spelling disaster for any AMC short position incurring the 200% fee rate. And the high price of put options makes synthetic routes equally unattractive.

So, perhaps a game of checkers is in order. While arbitrage traders play a complex tournament of hedging, ordinary investors will be better off playing the simple game of “buy the discounted APE shares.” In the best-case scenario, the APE/AMC marriage goes through and prices converge somewhere between $1.80 and $8. And in the worst-case scenario, the most you can lose is $1.80 per share.

Sounds like a decent win to me.

On the date of publication, Tom Yeung did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.