If you had $200 billion lying around, why wouldn’t you want to have your own bank?

That’s probably what Twitter CEO Elon Musk thought when he floated the idea of buying SVB Financial’s (NASDAQ:SIVB) subsidiary Silicon Valley Bank on March 11. Other tech and crypto moguls have since offered up plans of their own.

If you own SIVB stock, you might also love the idea of a massive takeover. Silicon Valley Bank shares must surely be worth something. And if a buyer is willing to overpay to have their name on the door, then investors should clearly take the deal.

But SIVB shareholders have instead found themselves stuck in regulatory hell (also known as a trip to the DMV). On the one hand, a bank sale to Mr. Musk or his contemporaries is political suicide for any regulator. They would much rather the failed bank merge with an existing one, even though no bidders have stepped up. But on the other hand, a pure liquidation of SVB’s assets without consideration for shareholders will surely spark class-action lawsuits. It would also raise the question of where any residual value should go.

So you hold SIVB stock… Now what?

Can You Sell SIVB Stock?

First, there’s the practical matter of transacting SIVB:

You can’t.

The Nasdaq exchange halted all trading in SIVB stock at 8:35 a.m. Eastern on March 10 with news pending. As of this writing, the halt remains in place.

The options markets also remain closed for the stock. Trading in that ring ended at 5 p.m. the day before, which means investors can’t hedge long positions or create new speculative ones.

That’s certainly bad news for Silicon Valley Bank shareholders. They might see SIVB’s stock listed at its last-quoted $106.04 price on their trading platform. But try to buy or sell the shares, and they’ll find themselves unable to make a transaction. (If it makes you feel better, I also have several “zeroed-out” stocks that will forever adorn my portfolio).

So, from a practical standpoint, there’s little to do except wait for any trading halt to lift.

What’s SIVB Stock Worth?

Then there’s a more difficult question:

Will SIVB stock become worth anything in the future?

That’s far harder to answer, and depends on who you ask.

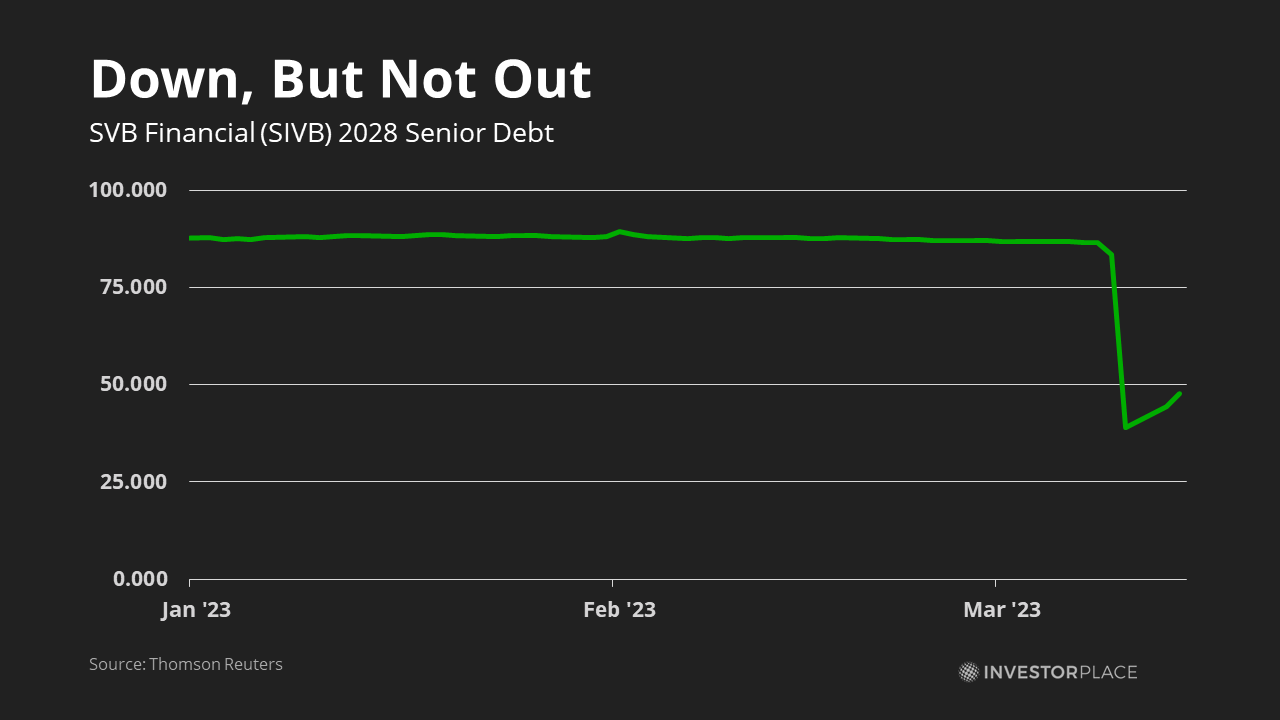

First are the bond markets, where SVB Financial’s debt continues to trade. On March 14, prices of the bank’s senior unsecured issues jumped to 50 cents on the dollar, their highest level this week. They’re priced even higher than the equivalent debt of meme stock AMC Entertainment (NYSE:AMC), and suggest SIVB stock could be worth as much as $80 per share. That represents a 70% haircut from SIVB’s undisturbed price — a typical discount we see when bond prices drop by half.

As a reminder, bankrupt firms will first compensate senior secured bondholders, then senior unsecured ones. Any remaining funds are then given to shareholders.

Then there’s a bottom-up analysis. That would take SIVB’s assets, subtract an appropriate discount for loan losses, and deduct senior liabilities from the figure. Whatever remains is the value that equity holders get.

Here, we quickly run into trouble. SIVB’s 2022 filings are now outdated by almost three months. And we know from a March 8 press release that the bank had sold around $21 billion of securities at a $1.8 billion loss.

That means the “appropriate discount” for other loan losses is an educated guess at best. At worst, it’s a recipe for a total misvaluation.

We can try anyway.

In SIVB’s most recent filings, the bank showed $173 billion in total deposits and around $20 billion in other senior obligations. That comes to roughly $193 billion of contractual obligations. Once you add contractual interest, the figure comes to around $195.5 billion. Next, SIVB posted $211.8 billion of assets in its most recent statement, leaving an equity cushion of $16.295 billion (the difference between assets and liabilities). A $1.8 billion loss reported last week reduces it to around $14.5 billion. So far, so good.

Now, we know that SIVB’s assets are far less than $211.8 billion since the bank took a significant loss on its $21 billion securities sale. A negative 8.6% margin, to be precise. If we apply that discount to the bank’s entire $211.8 billion, its asset value drops to $193.5 billion. (That’s 211.8 billion multiplied by 91.4%). And if that were the case, SVB Financial’s equity value is negative, and shareholders walk away with nothing.

The truth might be far worse. If losses approach 15% because of its assets’ illiquidity, the resulting fire sale will reduce SVB’s asset value to $180 billion. In this case, bondholders also walk away with zero. This is likely what U.K. regulators believed when they allowed the sale of SVB’s United Kingdom assets to get sold for 1 GBP to HSBC (NYSE:HSBC) on Monday.

But here’s where the bottom-up analysis also falls short. Silicon Valley Bank has significant off-balance sheet assets, including a nationwide network of branches, a (formerly) desirable brand name, and the human capital of its 8,500 employees, among others. A rival bank (or Elon Musk) could theoretically overpay for SIVB assets in hopes of recouping the loss somewhere down the line. In this case, investors will end up either with cash (unlikely) or shares of the purchasing bank (more likely).

What’s Next for SIVB Shareholders?

This optimism will prove cold comfort for anyone who owns SIVB stock. Shareholders have already sued SVB Financial and its management in hopes of recouping something… anything… from the defunct bank. They will join a long line of creditors waiting for a piece of the remaining assets.

Still, investors have a sliver of hope in recouping a portion of their losses. In the 2008 financial crisis, Wachovia Bank stockholders ended up with 0.1991 shares of Wells Fargo (NYSE:WFC) after the larger institution swooped in with an offer that outbid Citigroup’s (NYSE:C) expected takeover. And with SIVB’s bonds still trading for a non-zero value, credit markets seem to believe there’s plenty of value left in the parent of Silicon Valley Bank.

As with a trip to the DMV, there’s nothing to do but wait.

On the date of publication, Tom Yeung did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.