I wanted to find five stocks to buy with steady dividends and earnings that are reasonably cheap. Moreover, they each of these dividend stocks have attractive upside target prices.

This actually turned out to be harder to find than I expected. I finally found the stocks by setting a dividend and earnings screen that mirrored each other. This meant that I was looking for stocks to buy with greater than 20% earnings and 20% dividend growth. In addition, I looked for companies that were cheap with reasonably low price-to-earnings (P/E) ratios.

Lastly, I wanted to make sure the upside of the stock was at least 20%. I did this three ways. I used a historical dividend yield valuation technique, a historic P/E valuation method, and a peer comparable valuation method. By averaging all three methods to determine a target price, I was able to derive the upside for each stock.

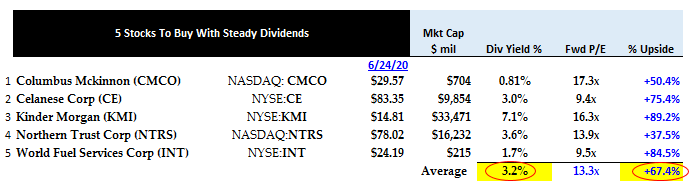

As a result, I found the following five dividend stocks to buy:

- Columbus McKinnon (NASDAQ:CMCO)

- Celanese Corp (NYSE:CE)

- Kinder Morgan (NYSE:KMI)

- Northern Trust (NASDAQ:NTRS)

- World Fuel Service (NYSE:INT)

Let’s dive and look at each of these stocks.

Dividend Stocks to Buy: Columbus McKinnon (CMCO)

Columbus McKinnon makes motion control products to move, lift, position, and secure materials. Key products include hoists, crane components, actuators, rigging tools, light rail work stations, and digital power and motion control systems.

Therefore its business depends on economic growth and industrial capex spending. Now that the U.S. seems to be slowly exiting a recession in consumer and business spending, its outlook for the future is picking up.

This $717 million market cap company has enjoyed steady growth in its dividends in the past four years, which you can see in the chart at the right.

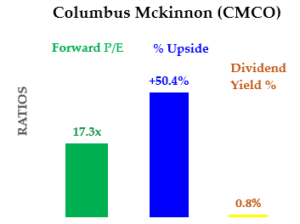

In addition, the present dividend yield of 0.75% is actually higher than its historical yield of 0.6%.

Analysts expect earnings for Columbus McKinnon to hit $1.71 per share in 2021, based on Seeking Alpha’s analysis. This represents growth of over 108% over 2020 expected EPS of 82 cents per share.

Based on its growth in earnings and dividends the company is likely to raise its dividend in the future.

Moreover, based on my assessment of its target value, the upside for the stock is over 50%. This is based on an average of its target values based on historic dividend yield, peer comp valuation, and historical P/E ratio analysis.

CMCO stock is cheap at 17x forward earnings, with a 50% upside, a steady dividend, and a 0.75% dividend yield.

Celanese Corp (CE)

This $10 billion market cap special materials and chemical company has paid a steady dividend over the past four years. You can see this in the chart below.

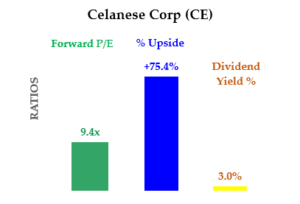

Moreover, the dividend yield for CE stock is attractive at 3% and represents very good value.

In fact, the company’s historical dividend yield over the past four years is lower at 2.01%, based on numbers from Seeking Alpha.

This is actually one of the methods I value the company. Based on this I estimate the stock is worth 48% more than today’s price.

Analysts expect the company to make a 30% growth in earnings per share in 2021 over 2020. That puts the EPS rate at $8.85 and gives CE stock an attractive P/E ratio of just 9.4 times.

Based on the company’s historic P/E ratio of 11.3 times, I estimate it is worth 20% more than today.

In addition, based on a comparable valuation of its peers, CE stock should trade at a much higher P/E ratio. I estimate at 24 times earnings the stock is worth 158% more than today.

On average, CE stock has an average target value of $146.21. This represents an upside potential for the stock of 75%. So, at a 10x P/E ratio, with a 3% dividend yield, and 75% upside, CE stock represents very good value.

Kinder Morgan (KMI)

Kinder Morgan is a $33.4 billion market cap natural gas pipeline and storage company, including liquefied natural gas. It is a massive midstream oil and gas company, operating 83,000 miles of natural gas pipelines and 147 terminals.

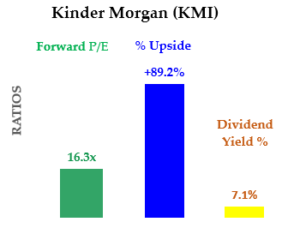

KMI stock has a very attractive dividend yield of 7.1% and has paid a steady dividend over the past years.

Based on its historical 4% dividend yield, KMI stock should be trading at $26.45 per share, an upside of over 78% from today’s price.

Moreover, in the company’s most recent conference call on its Q1 2020 earnings, a possible increase was discussed. Management expects to increase the dividend per share rate to $1.25 in January 2021.

KMI has plenty of FCF to cover the dividend. Its LTM FCF yield as of Q1 2020 was 8%. This is higher than the 7.1% dividend yield so the dividend is well covered. This looks like a solid high dividend yield stock.

Based on my analysis of its target value using its historical price-to-earnings ratio (35 times), KMI stock should be higher. I estimate its target value using this measure is 118% higher than today.

That is because I estimate the stock will make 91 cents per share in 2021. That gives the stock a P/E ratio of just 17 times earnings.

Moreover, based on an analysis of its peers’ P/E ratios, I estimate KMI stock is worth 71% more.

Therefore, combining all three of these valuation methods, the target value for KMI stock is $28.03 per share. That represents an upside of over 79% from the price today.

Given its low P/E and high and steady dividend yield, this represents an attractive investment opportunity.

Northern Trust Corp (NTRS)

Northern Trust is a wealth management, asset servicing, asset management, and banking solutions company with a $16 billion market value. It primarily serves institutions and high net worth clients.

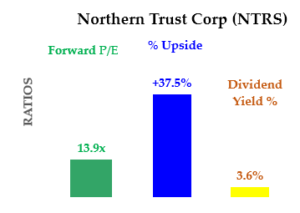

NTRS stock has an attractive 3.6% dividend yield and has a steady history of being paid, as can be seen in the chart below.

Moreover, based on its historical yield of 2.01%, the stock is worth $132.70, or 70% higher than today.

In addition, the historical P/E ratio for the company, based Value Line’s tear sheet on the company for the past five years is 15.8 times earnings. That is higher than today’s P/E ratio.

Therefore, this stock is worth 14% higher than today’s price. This is used in the final valuation target price for the stock.

In addition, based on a comparison with its peers, the stock is worth 28.5% more. This is because the peer comp P/E ratio is 17.8 times earnings.

On average, the target value for Northern Trust stock is $107.31 per share. This is 37.5% higher than today’s price.

Given the stock’s 3.6% dividend yield, its steady dividends, and its low P/E ratio, this is one of the best dividend stocks to buy and is attractive to most value investors.

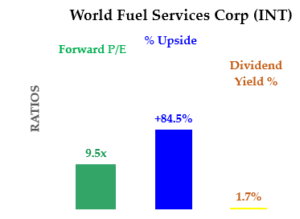

World Fuel Services (INT)

World Fuel Services is a $215 million market cap company that distributes fuel in the aviation, marine, and land transportation industries. Most of the company’s revenue from its aviation segment.

But the company actually was still profitable in all three segments in its most recent quarter. In fact, the land transportation fuel service segment posted the largest profit.

Right now the stock yields 1.58% and the company has paid a steady dividend as can be seen in the chart below and to the right. Seeking Alpha indicates that its dividend has grown 19.1% over the past five years.

Moreover, earnings in the year 2021 are expected to recover significantly as aviation travel begins to pick up again. Based on this, analysts estimate that World Fuel Services will have an 80% higher EPS growth in 2021.

Moreover, it sports a low 9.5x P/E ratio based on its expected 2021 earnings per share.

In effect, this is one of the stocks to buy based on a turnaround in the world economy. It is a play on an increase in fuel usage by plane, trains, ships, and large transportation vehicles.

Based on the company’s historical dividend yield, it should be worth over 94% more than today. The yield over the last four years was 0.80%, versus the 1.65% yield today, according to Seeking Alpha.

Moreover, average in its other valuation measures, including historical P/E ratios and peer-based P/E ratios, the stock is worth 84.5% more. That puts its stock value at $44.64 per share.

Given its attractive dividend yield and low P/E ratio, along with its 84% upside target, World Fuel Services stock is very attractive.

Summary

If you look at the table below, you see that the average dividend yield of this group of stocks to buy is 3.2%. Moreover, the average price-to-earnings ratio was very low at only 13.3 times.

The upside target on average for this group is over 67% from today’s prices. This represents the average of three methods of valuing each stock. These were comprised of a historic dividend yield target, a historic P/E ratio target, and a peer-based target.

The bottom line is you get paid to wait for the value to emerge. The dividend yield of over 3.2% annually represents a much better deal than you can get by leaving your money in the bank. In addition, you get all the upside potential of these dividend stocks.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. Mark Hake runs the Total Yield Value Guide which you can review here.